There is no doubt that the COVID-19 pandemic motivated health care providers, payers, and patients to adopt digital tools and contact-less services, allowing people to deliver and receive medical care.

Still, 18 months into the pandemic, now endemic and in its fourth wave of cases spiking around the world and in many parts of the U.S., some aspects of “digital transformation” seem not to have fully transformed American healthcare, we learn in HIMSS’s annual 2021 State of Healthcare Report. HIMSS collaborated with the organizations Trust Accenture, The Chartix Group, and ZS on this year’s research.

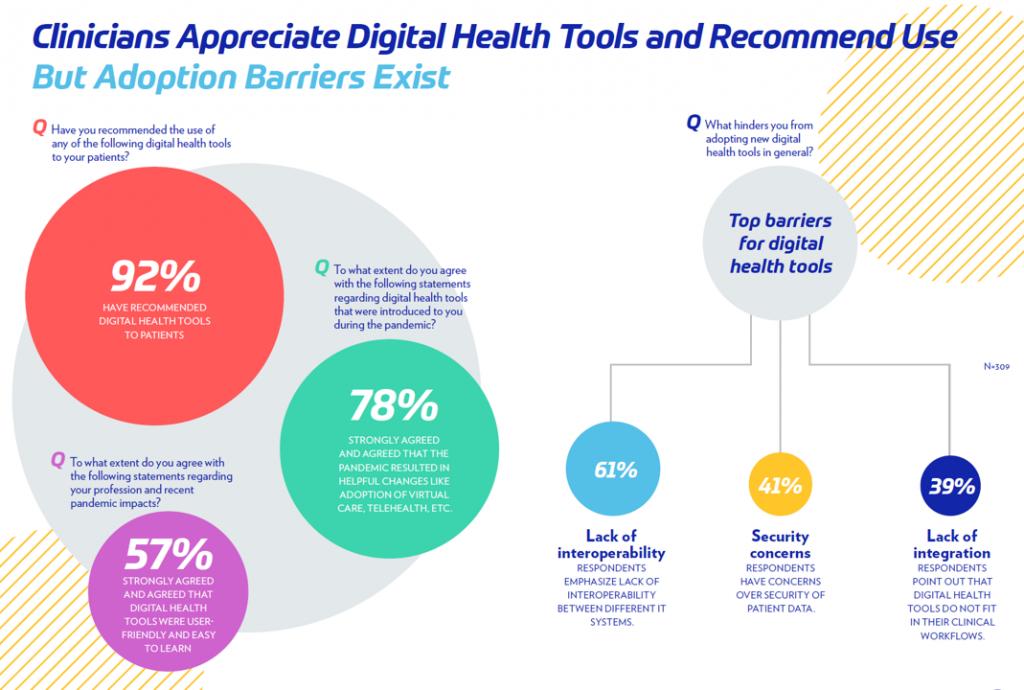

Nine in ten clinicians have recommended digital health tools to patients, and 8 in 10 clinicians strongly concurred that the pandemic resulted in helpful changes including the adoption of telehealth.

Nine in ten clinicians have recommended digital health tools to patients, and 8 in 10 clinicians strongly concurred that the pandemic resulted in helpful changes including the adoption of telehealth.

Still, the lack of interoperability remains a barrier hindering clinicians from using digital health tools. Security, too, remains a block with 41% of clinicians still concerned over the security of patient data.

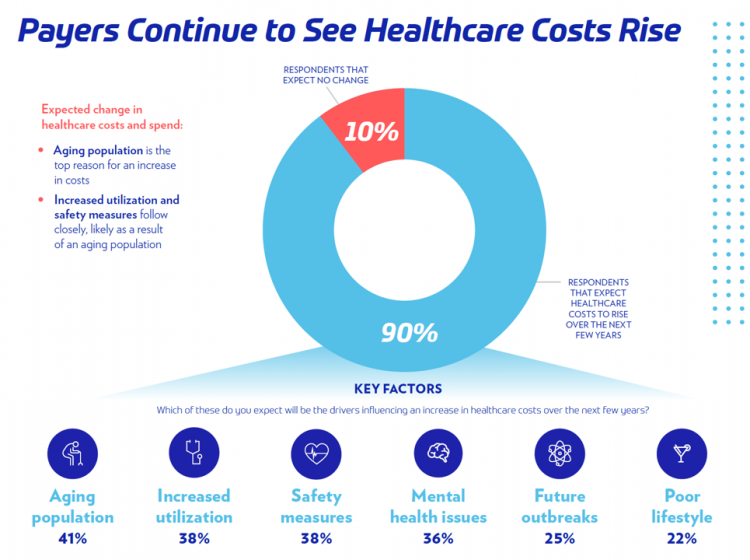

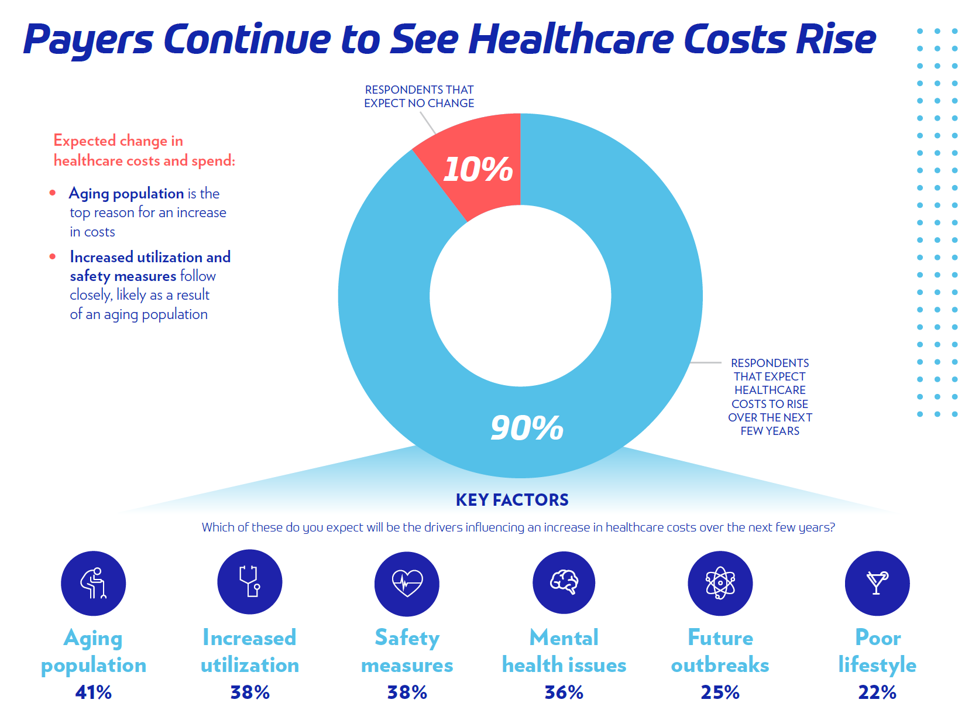

The study assessed payors’ perspectives in 2021, finding their top three concerned were increasing costs, quality of care, and the prospects for another pandemic. Payors’ identified the top factors driving health care costs up including an aging population, growing utilization of medical services, implementing safety measures (think: PPE and the ongoing challenge of adverse events), mental health (a growing epidemic inside the pandemic), possible future outbreaks, and (some) patients’ (unhealthy) lifestyles.

Payors also tend to think that stakeholders outside of “healthcare” per se — those so-called new entrants, like tech companies and Big Retail — will be the players who are more likely to innovate the industry compared with legacy providers and health insurance plans.

![]() The report found a generational split when it came to some patients wishing for healthcare to get back to “pre-COVID normal” and younger consumers favoring virtual care and contact-less options for services. In this study, one-half of patients had experienced at least one telehealth visit in the past year. Over one in three patients were using some form of wearable technology to track their health, a statistic consistent with other studies we’ve reviewed in the pandemic era.

The report found a generational split when it came to some patients wishing for healthcare to get back to “pre-COVID normal” and younger consumers favoring virtual care and contact-less options for services. In this study, one-half of patients had experienced at least one telehealth visit in the past year. Over one in three patients were using some form of wearable technology to track their health, a statistic consistent with other studies we’ve reviewed in the pandemic era.

Like payors, patients are very concerned about health care costs in the U.S., with 4 in 5 believing that costs in U.S. healthcare are too expensive.

Health Populi’s Hot Points: Unaddressed in this report on the “State of Healthcare” is an elephant in this room, and that is the continued endemic nature of the COVID-19 pandemic. After 18 months living and caring for patients with the coronavirus, and those both managing chronic conditions and those delaying care, The State of Healthcare in America is highly variable depending what ZIP code you live in, what health care insurance coverage you have (or whether you have it at all), whether you have access to broadband, your race and ethnicity, and whether you are a hands-on health care service provider.

If you are the latter, and especially on the frontlines of COVID-19 in intensive, critical, and respiratory care hospital wings, when you are pretty burned out and frustrated with millions of people in the U.S. who have chosen not to get vaccinated yet, and not planning to do so. As of today, only one-half of people in the U.S. have been fully vaccinated.

Today, parts of the U.S. are COVID hotspots again: the state of Florida is there, and Nevada — where the HIMSS conference will meet in person beginning exactly two weeks from today — has a fast-growing burden of patients in hospitals due to the coronavirus.

As we plan for The State of Healthcare in 2022, we can identify a few certainties on which we can count, if soberly and pragmatically:

- More patients will seek care on their own terms as the fourth wave of COVID-19 will find those risk-averse patients demanding services at-home or closer-to-home in their local communities (think: retail health, urgent care, care via mobile vans in rural areas, and of course, telehealth demands should rise again)

- Patients who delayed care in 2020 will present to their providers with worse conditions — say, cancers moving from Stage 1 or 2 to Stage 3, or muscle tone atrophied due to delayed physical therapy

- Mental health and behavioral health issues will continue to be the epidemic inside the COVID-19 pandemic, presenting as a single condition (particularly in younger people) and as a co-morbidity with other conditions (like diabetes, heart disease, gut issues, et. al.); and, caregiver stressors will continue to plague millions of health citizens

- The cost of health care, and especially for prescription drugs, are squarely in the sights of both patients and payors. This issue will be in the eyes of bipartisan legislators looking to the 2022 mid-term elections

- Security and privacy are on the minds of both clinicians and patients, while payors and other stakeholders looking to gather even more data on patients via wearable tech, Internet of Things devices, and third-party data brokers’ mines of retail and other data. Watch for the tech antitrust policymakers and regulators to work in parallel as AI and machine learning need more data to work well and equitably. This issue will require a lot of education among all the stakeholders involved — from patients and citizens to policymakers.

The annual 2021 HIMSS Global Conference will be meeting in Las Vegas, Nevada, the week of August 15th. I won’t be there in person, opting in to the digital program in lieu of attending face-to-face. Stay tuned for my usual observations from the Conference, this year so profoundly shaped by the pandemic, growth of cloud computing, burned-out clinicians, and impatient patients.

Thank you

Thank you  Jane joined host Dr. Geeta "Dr. G" Nayyar and colleagues to brainstorm the value of vaccines for public and individual health in this challenging environment for health literacy, health politics, and health citizen grievance.

Jane joined host Dr. Geeta "Dr. G" Nayyar and colleagues to brainstorm the value of vaccines for public and individual health in this challenging environment for health literacy, health politics, and health citizen grievance.