The top 25 life science companies grew a paltry 1% in 2014, and 70% of recent brand launches underperformed analysts’ expectations.

The introductory page of a new report from KPMG describes, in a single sentence, the very challenging market environment for bio/life sciences:

“The pharmaceutical industry is caught between a blockbuster-driven past and a future comprising precision medicine, curative therapies, and payment for outcomes. The years of consistent double-digit growth and unconstrained pricing power are fading into memory.”

The assertively titled, “Change in pharma? Not optional,” offers 10 “integrated imperatives” for the pharma industry to follow to best respond to the challenges of value-based payment and precision medicine. They are:

- Be more tactically commercial, less clinical

- Take pricing and contracting to the top of the organization

- Be more holistic in stakeholder mapping

- Base sales on a collaborative approach to improving patient outcomes

- Play a larger role in the industry moving from volume-to-value

- Support healthcare providers in improving quality and patient satisfaction

- Leverage data and analytics to support commercial strategies

- Allocate commercial resources better across markets and brands

- Evolving performance metrics and incentives to align with this new world of value

- Adopt these strategies through the enterprise.

Bio and life science companies must deal with the current commercial/market realities: declining physician access (namely, clinician prescribers closing doors to live, in-person meetings with sales forces; increasing regulatory (especially FDA) complexity; and, growing patient engagement in making clinical and financial decisions for themselves given their adoption of high-deductible health plans, HSAs, and self-payment.

Health Populi’s Hot Points: In the past two weeks,  two major prescription benefit management companies (PBMs) announced their formulary cuts. These announcements make KPMG’s strategic imperatives all the more important and impactful.

two major prescription benefit management companies (PBMs) announced their formulary cuts. These announcements make KPMG’s strategic imperatives all the more important and impactful.

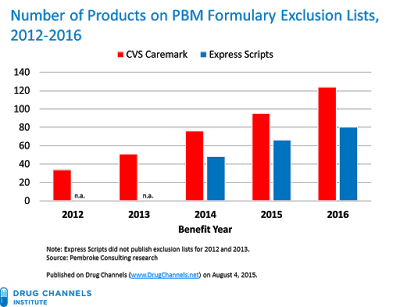

As the Drug Channels Institute’s Adam Fein observed, “the lists keep getting longer.” The Institute published the bar chart which illustrates the two PBMs’ formulary cuts.

Express Scripts, the #1 PBM, announced its 2016 National Preferred Formulary on July 31 2015. It’s the most widely-used drug list in the U.S., covering 25 million Americans. The company wrote, “out of more than 4,000 drugs available on the market, we will offer a formulary that excludes 80.” These include the Hepatitis C drugs Sovaldi and Harvoni (discussed here in Health Populi), AstraZeneca’s Onglyza (for diabetes), and Qysimia (a weight loss drug). Express Scripts estimates they will save $1.3 bn with these cuts.

CVS Health, which owns Caremark, the second-largest PBM, cut 31 prescription meds from coverage for 2016. The biggest name brand eliminated from coverage is Viagra, along with some popular therapies for diabetes and multiple sclerosis. (BTW, Viagra, which sold $1.8 bn in 2014, is expected to go generic in December 2017).

While PBMs will continue to play a role in building the menu from which patients can benefit, patients-as-consumers will grow as a force in determining what therapies they want to benefit from. As specialty drug prices present sticker shock to consumers who pay a growing share of higher-and-higher priced therapies, we will see growing tension between the quadrangle relationship of patients, doctors, PBMs and life science companies.

Thank you

Thank you  Jane joined host Dr. Geeta "Dr. G" Nayyar and colleagues to brainstorm the value of vaccines for public and individual health in this challenging environment for health literacy, health politics, and health citizen grievance.

Jane joined host Dr. Geeta "Dr. G" Nayyar and colleagues to brainstorm the value of vaccines for public and individual health in this challenging environment for health literacy, health politics, and health citizen grievance.