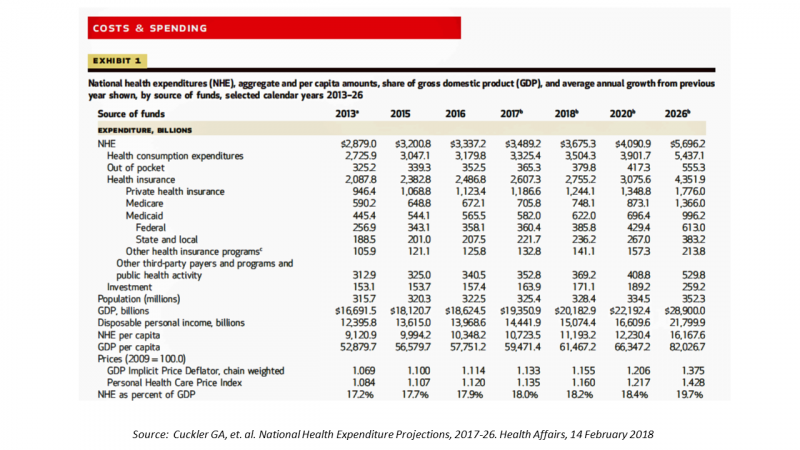

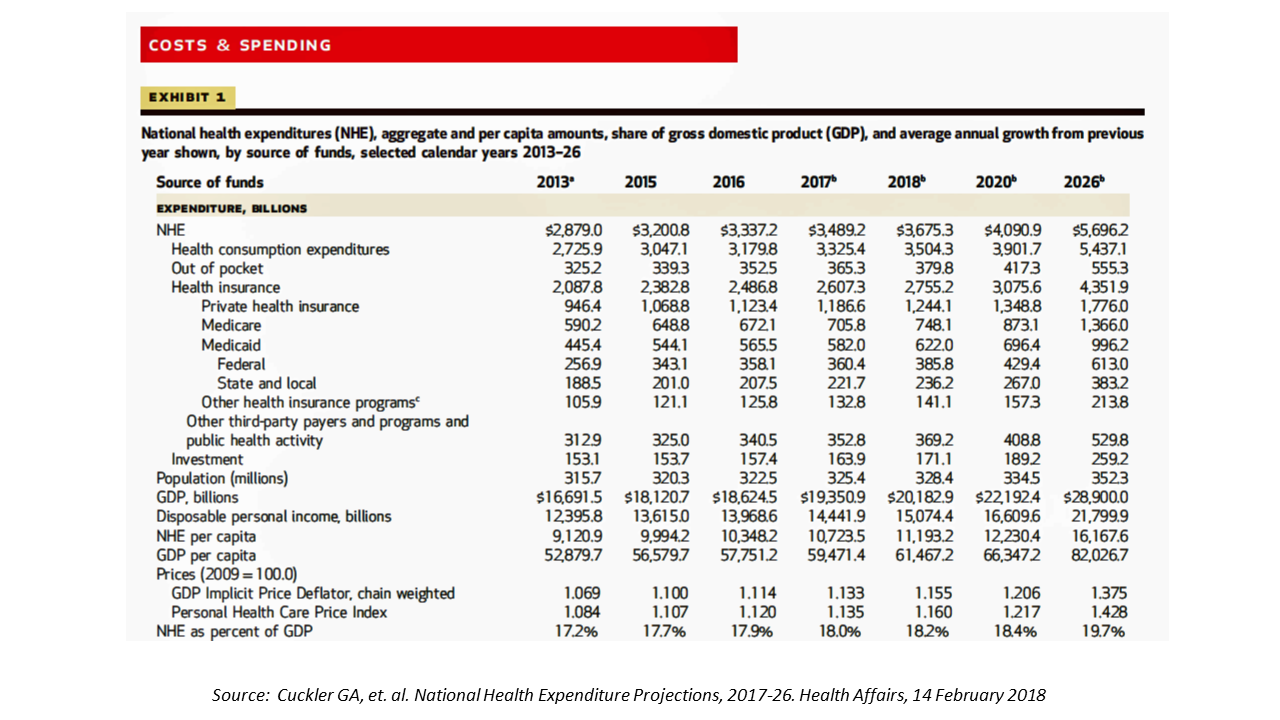

In 2020, national health expenditures (NHE) in the United States will exceed $4 trillion to cover 334.5 million Americans. That equates to 18.4% of the Gross Domestic Product (GDP) and $12,230.40 of health spending per person.

I sat in on a press call today with researchers from the Office of the Actuary working in the Centers for Medicare and Medicaid Services (CMS) to review the annual forecast of the NHE, published in Health Affairs in a statistically-dense eleven page article titled, National Health Expenditure Projections, 2017-2026: Despite Uncertainty, Fundamentals Primarily Drive Spending Growth.

I sat in on a press call today with researchers from the Office of the Actuary working in the Centers for Medicare and Medicaid Services (CMS) to review the annual forecast of the NHE, published in Health Affairs in a statistically-dense eleven page article titled, National Health Expenditure Projections, 2017-2026: Despite Uncertainty, Fundamentals Primarily Drive Spending Growth.

What are those “fundamentals” pushing up healthcare spending? Three factors will drive healthcare costs to 2026: prices for medical goods and services, changes in income growth, and shifting enrollment from private health insurance to Medicare — driven by the aging of Boomers.

Focusing in on the health insurance line item, 44% will be covered by private/commercial payors and 51% by Medicare and Medicaid (the remaining 5% of insurance costs will lie with other third-party payors and programs).

The annual growth rate of medical spending will be 5.5% per year, 2017-26, expected to hit $5.7 trillion in 2026 when healthcare spending will be $1 in every $5 in the American economy (approaching 20%). That 5.5% is also 1% faster than expected GDP growth.

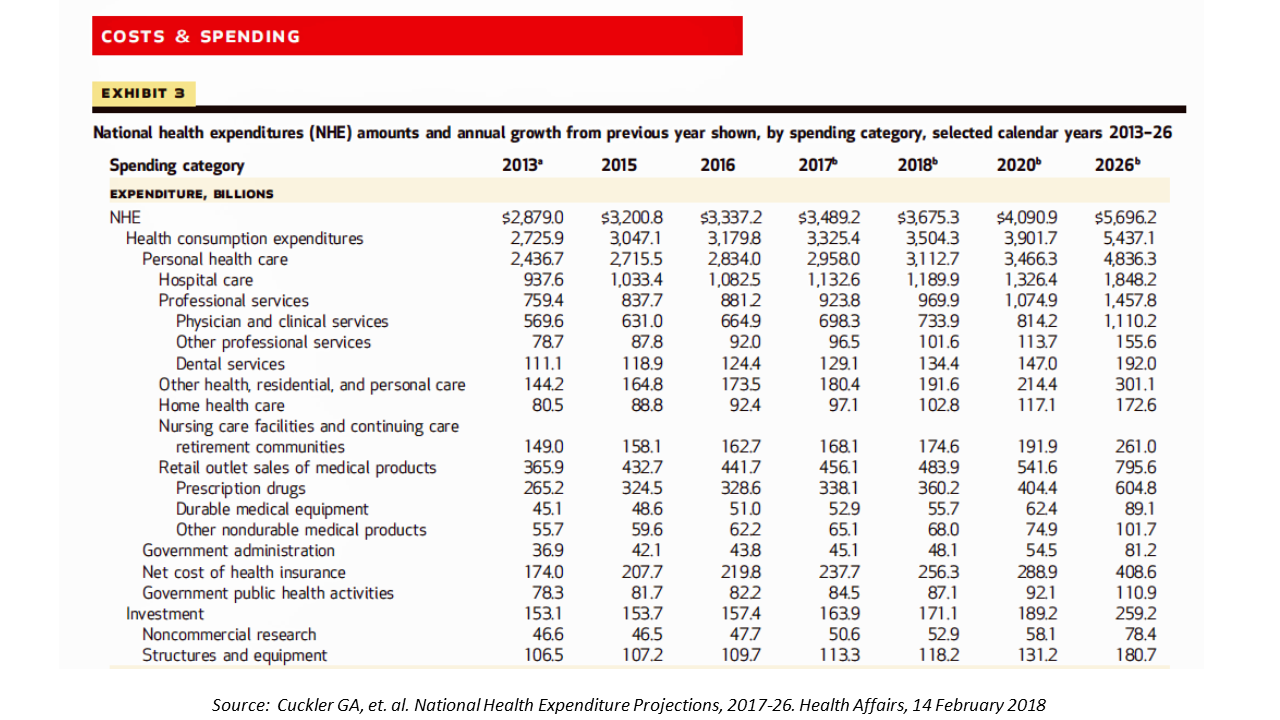

The second table details medical spending by category: hospital care, professional services (doctors, dentists, and other professionals), residential and personal care, home care, long-term care, and the retail sales of medical products: namely, prescription drugs, durable medical equipment, and disposable supplies. The three largest line items of NHE in 2020 will be:

The second table details medical spending by category: hospital care, professional services (doctors, dentists, and other professionals), residential and personal care, home care, long-term care, and the retail sales of medical products: namely, prescription drugs, durable medical equipment, and disposable supplies. The three largest line items of NHE in 2020 will be:

- Hospitals = $1,326 trillion = 38% of NHE

- Professional services = $1,075 trillion = 31% of NHE

- Prescription drugs = $404 trillion = 11.6% of NHE.

Together, these three categories will comprise just over 80% of health spending in 2020.

Health Populi’s Hot Points: Prices of services and goods continue to be a key cost driver in American healthcare, which is old but continuing news that the CMS forecast assumes in its financial model.

Altarum Institute informed a story in Bloomberg news yesterday on the end of a long-run of low-cost increases in U.S. healthcare. The third chart on “price hikes slow” illustrates the low-growth medical cost story since the start of the Recession.

Altarum Institute informed a story in Bloomberg news yesterday on the end of a long-run of low-cost increases in U.S. healthcare. The third chart on “price hikes slow” illustrates the low-growth medical cost story since the start of the Recession.

If that slow-growth cost scenario is over and the U.S. faces the next few years of 5.5% growth rates, reflected in today’s CMS forecast, we face personal health care price inflation that will exceed general price inflation in the U.S. economy.

The CMS team added a “special topics” section at the end of the forecast report with an analysis of prescription drug rebates and specialty drug price impacts, and a discussion about the effect of high-deductible health plans (HDHPs) on national health spending.

Over one-quarter of American workers were enrolled in HDHPs in 2017, Kaiser Family Foundation found in their annual employer health benefit survey. Consumers’ enrollment in HDHPs has been found to lower their demand (use, utilization) of health care services and goods (such as prescription drug fills or continuation). This self-rationing behavior has resulted in a deceleration in private health insurance spending growth for hospital care and physician services, the CMS team points out.

![]() Through the eyes of the American patient, now health consumer, affordability continues to rank ahead of quality or access for health care based on TransAmerica’s research into healthcare consumers in a time of uncertainty. Underpinning affordability concerns is 70% of consumers’ confession that they do not currently save for healthcare expenses.

Through the eyes of the American patient, now health consumer, affordability continues to rank ahead of quality or access for health care based on TransAmerica’s research into healthcare consumers in a time of uncertainty. Underpinning affordability concerns is 70% of consumers’ confession that they do not currently save for healthcare expenses.

Savings rates have hit a low in 2018 for Americans, consumer debt continues to creep up, and health care prices will drive medical spending over the next several years. The U.S. consumer will continue to face medical cost affordability challenges and will be at-risk of further self-rationing care if health plan sponsors — in both commercial plans funded by employers and public sector plans at the Federal and State level — do not artfully alter health plan benefit designs that nudge consumers-as-patients — to spend health dollars when they should — and patients-as-consumers, to understand what value-based healthcare means for their household in their healthcare communities.

This will impact patients’ financial relationships with hospitals and physicians, who will need to pay growing attention to revenue cycle management in even more risk-managing and creative ways. Someone in my social circle told me earlier today that they will be starting up a GoFundMe page soon to help them cover costs for an unexpected cancer diagnosis. We must never lose sight of the patients underneath numbers like $4 trillion of health spending, and what our ROI is on that spending through both public and individual health lenses.

Thank you

Thank you  Jane joined host Dr. Geeta "Dr. G" Nayyar and colleagues to brainstorm the value of vaccines for public and individual health in this challenging environment for health literacy, health politics, and health citizen grievance.

Jane joined host Dr. Geeta "Dr. G" Nayyar and colleagues to brainstorm the value of vaccines for public and individual health in this challenging environment for health literacy, health politics, and health citizen grievance.