Most consumers look to every industry sector to help them engage with their health.

Most consumers look to every industry sector to help them engage with their health.

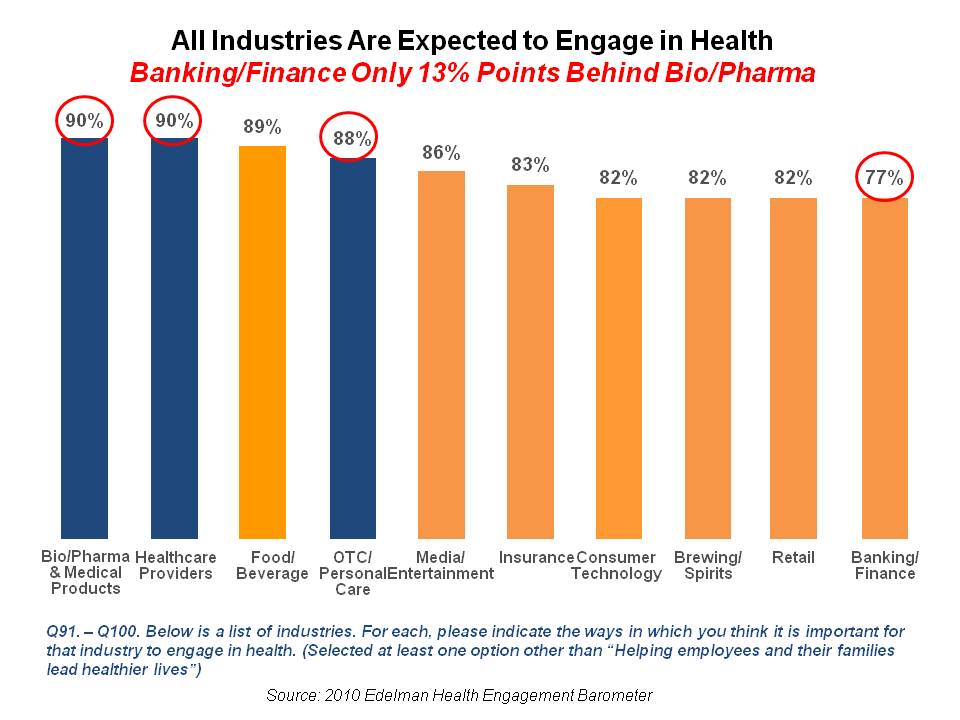

And those companies include the insurance industry and financial services firms, we found in the 2010 Edelman Health Engagement Barometer.

John Hancock, which covers about 10 million consumers across a range of products, is changing their business model for life insurance. Here’s the press release, titled, “John Hancock Leaves Traditional Life Insurance Model Behind to Incentivize Longer, Healthier Lives.”

“We fundamentally believe life insurers should care about how long and well their customers live. With this decision, we are proud to become the only U.S. life insurance company to fully embrace behavioral-based wellness and leave the old way of doing business behind,” Marianne Harrison, John Hancock president and CEO, said in the press release.

This is not a new-new thing for the life insurer: I wrote about John Hancock’s initial foray into so-called “behavioral-based wellness” with Vitality here on Health Populi in April 2015. Note that was over 3 years ago, so this approach has been well-honed and -tested over time.

Since working with Vitality, John Hancock’s policyholders have taken nearly two times as many steps as average American adults, and have engaged with the company, on average, over 1.5 times a day per year — versus other insured customers with traditional health insurance (that is 576 times a year versus 1 to 2 times).

The financial bottom line is that participants in the program experienced 30% lower hospitalization costs versus other insureds, and appear to live many years longer than others.

The financial bottom line is that participants in the program experienced 30% lower hospitalization costs versus other insureds, and appear to live many years longer than others.

John Hancock will offer two programs allying with Vitality: Vitality GO, bundled (for free) into all future life insurance policies. Insureds in GO will be able to freely download an app and use a web portal with health, fitness and nutrition advice, able to set and track personal goals. By participating in the tracking program, consumers can earn rewards for discounts, such as those shown in the illustration here.

The second program Vitality PLUS, is a premium version of the plan, costing enrollees $2 a month for single life premium plans, or 3% of the policy’s premium for other plans. In addition to the app and portal access, these insureds earn additional rewards and discounts, and potential premium savings up to 15% annually.

The Apple Watch and Fitbit trackers can be used among other wearable tech devices for the program.

These offerings will begin to be marketed to consumers in 2019.

Health Populi’s Hot Points: The health/care ecosystem continues to morph, with data-tracking-and-sharing, along with behavioral economics, baked into consumer-facing healthcare products and services. This is all about behavior change, and nudging (perhaps forcing) consumers to take on more responsibility: for financial and clinical decisions. Privacy, too, is a question in this and other data-sharing programs. Not only do wearable tech devices “leak” data that many consumers assume to be kept secure, but what about the opt-in for the insurance programs? What if a consumer wants to share certain data, but not other personally-generated information from, say, the bedroom or bathroom?

Health Populi’s Hot Points: The health/care ecosystem continues to morph, with data-tracking-and-sharing, along with behavioral economics, baked into consumer-facing healthcare products and services. This is all about behavior change, and nudging (perhaps forcing) consumers to take on more responsibility: for financial and clinical decisions. Privacy, too, is a question in this and other data-sharing programs. Not only do wearable tech devices “leak” data that many consumers assume to be kept secure, but what about the opt-in for the insurance programs? What if a consumer wants to share certain data, but not other personally-generated information from, say, the bedroom or bathroom?

In the case of John Hancock, we see the disruption of a 156-year-old company looking to become more relevant and attractive to a generation of younger people who may not be that keen on the concept or product called “life insurance.” That generation may not be as sensitive to the privacy concerns of, say, Boomers or Greatest Generation consumers.

But discounts, rewards, gamification and wearable tech? That’s a Millennial value proposition at work.

And don’t forget that Amazon Prime membership.

Most Millennials don’t see the value of life insurance, a Life Happens + LIMRA survey found.

The John Hancock announcement coincided with one from Fitbit, the dominant fitness wearable supplier which helped to define the category. Fitbit expanded Fitbit Care, a program to work with employers looking to bolster wellness among workers. Fitbit has invested in a technology platform to scale this offering. The company already works with employers’ wellness programs, and this development builds on that service, which grew with the company’s acquisition of Twine Health earlier this year to support Fitbit’s health coaching capabilities.

Just don’t get Twine Health confused with Twine, a financial wellness subsidiary of John Hancock.

Just don’t get Twine Health confused with Twine, a financial wellness subsidiary of John Hancock.

Thank you

Thank you  Jane joined host Dr. Geeta "Dr. G" Nayyar and colleagues to brainstorm the value of vaccines for public and individual health in this challenging environment for health literacy, health politics, and health citizen grievance.

Jane joined host Dr. Geeta "Dr. G" Nayyar and colleagues to brainstorm the value of vaccines for public and individual health in this challenging environment for health literacy, health politics, and health citizen grievance. {kind=link}