In American health economics, there’s a demand side and a supply side. On the demand side, we’ve done a poor job trying to nudge patients and consumers toward rational economic decision making, lacking transparency, information symmetry, and basic health literacy. On the supply side, we’ve engaged in a medical arms race allocating capital resources to shinier and shinier new things, often without cost-benefit rationale or clinical evidence.

On that supply side, though, I met up with an innovation that can help to bend the capital cost curve of how we envision and build new hospitals and clinics.

This week, I had the opportunity to tour, and participate in the ribbon-cutting launch of, MedModular, developed by EIR Healthcare.

This is a pre-fabricated structure that can be purposed as a single hospital bed room, an imaging pod, a clinical laboratory set-up, or any permutation for healthcare delivery.

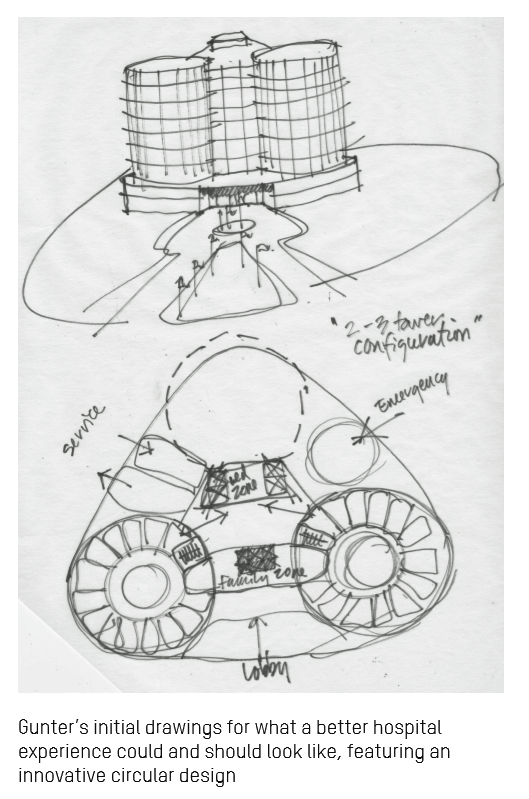

This concept was inspired by back-of-napkin drawings in the hand of Gunter Geiger, father of EIR Healthcare founder Grant Geiger.

Grant’s Dad had a keen design eye and worked with Knoll and Ford Motor Company. Gunter had a vision for a “circular hospital” that could deliver on enchanting user-centered design, productive workflow, and enchanting healthcare environment and experience for all stakeholders. You can see his sketches here.

Many of us who choose to work in the health/care ecosystem do so based on a personal experience. This is the case with Grant, whose father’s hospital experience as a patient informs and motivates the son’s realization of MedModular.

In healthcare, being smart and mission-driven at the same time requires addressing the Quadruple Aim: those four pillars are to enhance the healthcare experience, to bolster health outcomes, to support clinicians (doctors, nurses, allied professionals) in their daily work and prevent burnout, and to lower per-patient costs.

The economic argument for the MedModular innovation in the U.S. is compelling. Start with the fact that America will allocate $3.7 trillion to national healthcare spending in 2018.

Healthcare payors who foot the bill will be very interested to know about this development. This week, Kaiser Family Foundation published its 2018 study into employer-sponsored benefits, finding that the average cost is about $20,000 this year. Earlier this year, the Milliman Medical Index gauged a PPO for a family of four at $28,166.

That payor is the employer, indeed, for at least half of U.S. patients. But increasingly, the payor is also the patient-consumer, spending more out-of-pocket and first-dollar on premiums and high-deductibles, this year’s KFF research pointed out.

As payors, healthcare consumers have a high benchmark for customer experience that we have found in retail, in grocery stores, at banks, and of course online. Our customer experience expectations have been re-wired: we expect, even demand, that delightful retail experience from our providers, health insurance plans, pharmacies, and other healthcare touch-points.

We demand that from the supply side of U.S. healthcare for which we, as taxpayers and consumers, spend $3.7 trillion a year. Where does that money go?

We demand that from the supply side of U.S. healthcare for which we, as taxpayers and consumers, spend $3.7 trillion a year. Where does that money go?

The largest proportion, 32%, gets spent on hospital care. That equates to about $1.2 trillion in 2018.

I explained in my keynote speech at the MedModular launch that $1.2 trillion amounts to the entire GDP of Spain in 2017.

You should know that Spain allocates 9% of its GDP on healthcare – one-half of the per capita amount that the U.S. spends. And the OECD rates Spain as having the best health outcomes in the European Union in terms of life span, infant mortality, and quality of life.

In comparison, the U.S. healthcare spend is double Spain’s investment allocation has a miserable return-on-investment.

So how to bend the ever-increasing U.S. healthcare cost curve and improve health outcomes at the same time?

We must address this on multiple fronts, both on the demand side (for patients and physicians) and on the supply side of providers, plans, and suppliers. Here is where we can pay for, incentivize and build new models of care and support more productive, energizing workflows that result in better experiences for both clinicians and patients, and consume fewer resources at the same time.

Those resources are money (initial capital outlay and ongoing maintenance costs), time, and labor. They are also in the form of bolstering hygiene, as the surfaces in MedModular incorporate DuPont’s Corian which rejects the growth of bacteria, mold and mildew.

The room is cleaner, greener, smarter — features that today’s consumer, in and beyond healthcare, seek.

When we think beyond the initial building and capital outlay, healthcare can also can benefit from a lower cost of operating considering MedModular’s modular ability to adapt to changing demands, technologies, workflows, and public health wild cards like natural disasters and viral epidemics.

Health Populi’s Hot Points: At the MedModular launch, it was a delightful surprise for me to be followed by a speaker from the Disney Institute, Chuck Salvo, who spoke to the customer experience secret sauce that healthcare consumers expect and deserve — for both the pure experience and delight, but also for supporting optimal patient outcomes.

Health Populi’s Hot Points: At the MedModular launch, it was a delightful surprise for me to be followed by a speaker from the Disney Institute, Chuck Salvo, who spoke to the customer experience secret sauce that healthcare consumers expect and deserve — for both the pure experience and delight, but also for supporting optimal patient outcomes.

The Disney experience is indeed one of many consumers’ benchmarks for excellence and delight. In fact, the Disney Institute has worked for decades with healthcare organizations to bring that ethos to patients, clinicians, and communities.

I segue naturally now from Disney to LEGO: the press release for the MedModular launch uses the phrase, “LEGO-Esque.”

In my concluding remarks at this event, I noted the origin of the name LEGO. The family-owned company is based in Denmark, and the brand name “LEGO” was derived back in 1934 from the joining of two Danish words: “leg godt.” In English, that translates to, “Play Well.”

MedModular has the promise of re-imagining and -inventing lower-cost, better quality healthcare that can help us all play well in the ever-morphing healthcare ecosystem.

I'm gratified to be named on

I'm gratified to be named on  I’m celebrating America’s 250th birthday both patriotically and professionally, honored that the NLM included my 2010 paper, “How Smartphones Are Changing Healthcare for Consumers and Patients” as one of 250 items curated for the digital archive of 250 Years of American Medicine.

I’m celebrating America’s 250th birthday both patriotically and professionally, honored that the NLM included my 2010 paper, “How Smartphones Are Changing Healthcare for Consumers and Patients” as one of 250 items curated for the digital archive of 250 Years of American Medicine.