“Partnerships, including JVs and alliances with other healthcare organizations and with new entrants, are just one way to access new capabilities, unlock speed to market, and achieve capital, scale, and operational efficiencies” in health care transformations. “In an environment with continued competition for attractive assets and significant capital in play from institutional investors, these partnerships may also be the most accessible way for organizations to capture value in expanding healthcare services and technology value pools,” we learn in Overcoming the cost of healthcare transformation through partnerships from a team of health care folks with McKinsey & Company.

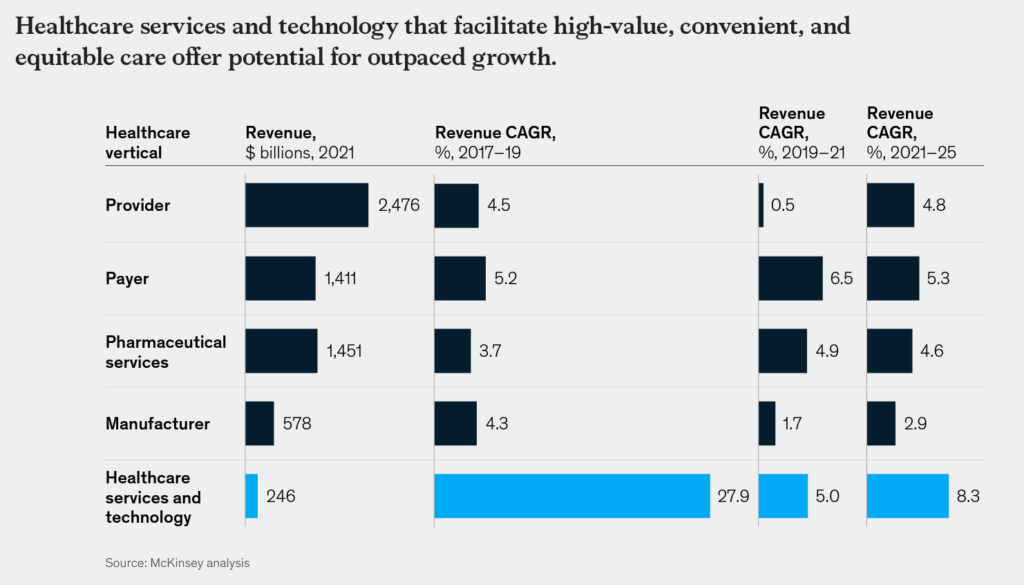

McKinsey portrays the vertical health care segments in this first graphic, detailing each area’s revenue and growth. Providers, payers, and pharma comprise the bulk of revenue. But see that health care services and technology, while a tiny segment today, will be fast-growing going forward — and a key enabler for transforming health care.

What fuels that transformation is data and the insights the right data can generate. And that data will be generated from many sources, frequently siloed and decentralized which can prevent aggregation, mash-up, and analysis.

In particular, the volume of health data from wearables, implantables, and other decentralized technologies is growing by 48% annually, according to a recent report from the Swiss Re Institute. That report spoke to the importance of connecting the disconnected health care landscape, including primary care, pharmacy, diagnostics, secondary care/hospitals, health technology providers, insurers, and information stewards, among other stakeholders in the fragmented health/care ecosystem.

We’re talking about a team sport here — to most effectively benefit patients’ outcomes from prevention through diagnosis and treatment. No one player — not even the ever-integrating and -acquisitive organizations like UnitedHealth Group, CVS Health, or Amazon — can go this alone.

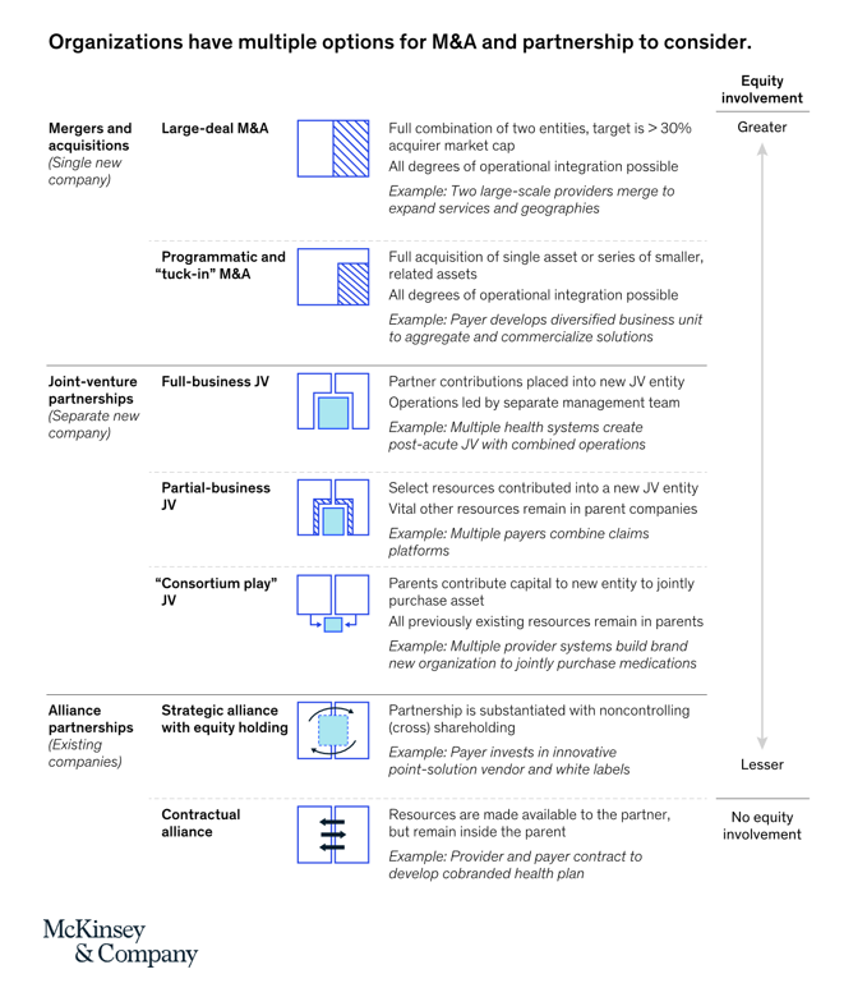

It will take partnerships and alliances to come together, and they can do so in a variety of ways, some shown in the second graphic from the McKinsey paper.

Beyond merging and buying (M&A), stakeholders in health/care can strike joint venture partnerships that are tight and former, partial, or so-called “consortium plays,” McKinsey describes. They offer the example of several health care providers coming together to contribute capital and purchase medications to bolster hospitals’ supply of scarce medicines.

Health Populi’s Hot Points: With even less capital and equity participation, partners can develop alliances via contracts to, say, co-brand a health plan or develop a population health program with consumer engagement through self-care, the bottom of McKinsey’s graphic just above illustrates.

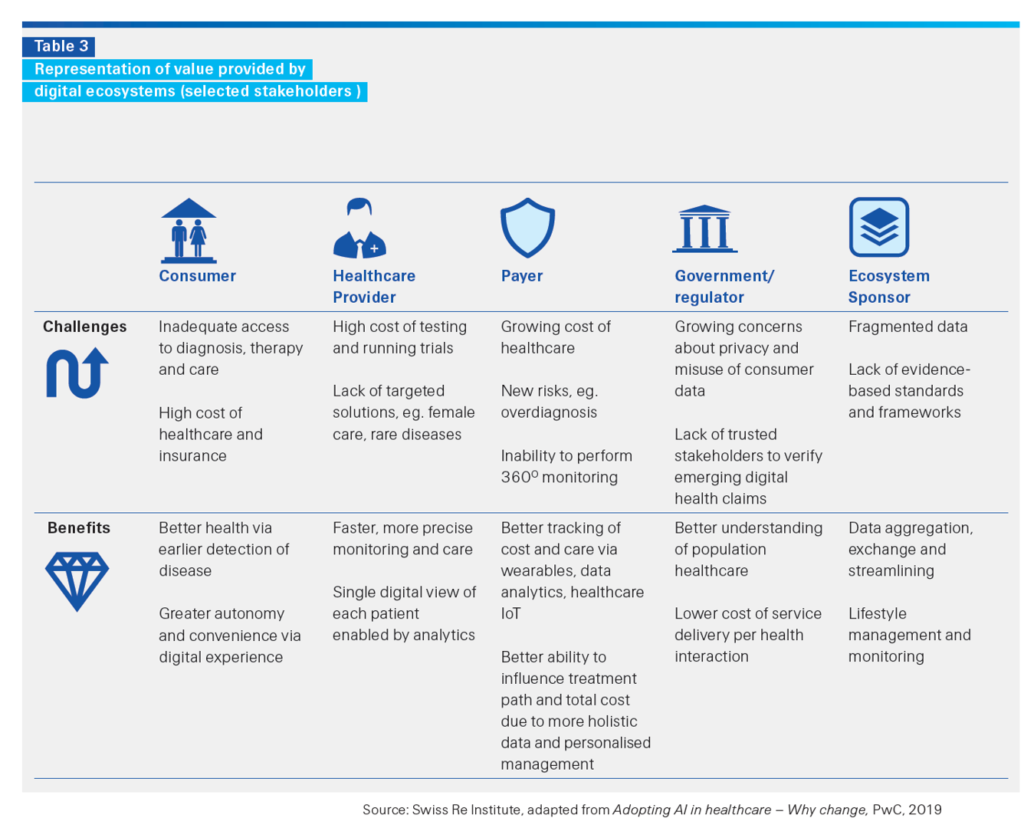

Here’s a table from the Swiss Re report to which I referred earlier, on how health ecosystems can enchant and streamline with patient experience.

Swiss Re, as a re-insurer, is in the business of managing risk. In the case of healthcare, connecting systems and people up with the right data at the right time can make big differences along the continuum of thriving living, disability, and death.

The Swiss Re table calls out five stakeholder groups, one of which was not called out in the McKinsey analysis: collaborating with consumers/patients.

As we look to partner across the health/care ecosystem to positively shape and impact patient journeys and outcomes, data will play a key role in doing so — especially data generated at the site of the person herself through wearables and other sensor-embedded devices and Internet-of-Things things at home, in our cars, and on-the-go.

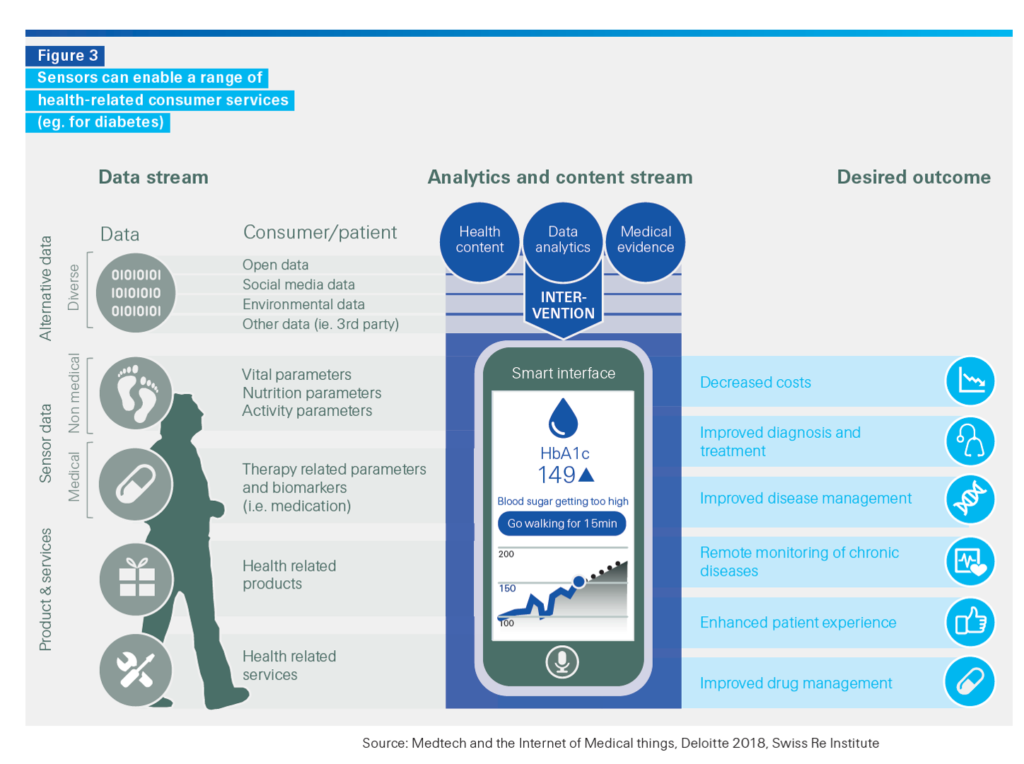

This last chart, from the Swiss Re report adapted from a version in a Deloitte study, diagrams examples of sensor data streaming for a patient dealing with diabetes.

In thinking holistically about effective management of chronic conditions through self-care of patients partnering with providers, health plans, and other organizations, we can imagine the ecosystem even more broadly through:

- Nutrition and food with grocery stores and pharmacies

- Fitness collaborations with YMCAs and connected gyms that can scale exercise to us in our hands and homes

- Pharma and life science companies to deliver holistic solutions for consumers’ self-care with digital companion apps, nutrition and exercise guidance that can complement medicines and bolster the drug’s benefits

- Financial guidance for managing health care costs (say, for co-sharing payments for specialty drugs),

and other touchpoints that support peoples’ everyday lives and health flows. Remember that value-based care works best when aligned with patients’ and providers’ values.

I'm gratified to be named on

I'm gratified to be named on  I’m celebrating America’s 250th birthday both patriotically and professionally, honored that the NLM included my 2010 paper, “How Smartphones Are Changing Healthcare for Consumers and Patients” as one of 250 items curated for the digital archive of 250 Years of American Medicine.

I’m celebrating America’s 250th birthday both patriotically and professionally, honored that the NLM included my 2010 paper, “How Smartphones Are Changing Healthcare for Consumers and Patients” as one of 250 items curated for the digital archive of 250 Years of American Medicine.