With valuations of digital health companies expected to decline in 2023, investors in the sector are Missourian in spirit in “Show Me” mode: here, it’s all about the clinical evidence and ROI, according to a survey from GSR Ventures. conducted among over 50 major digital health venture capital investors.

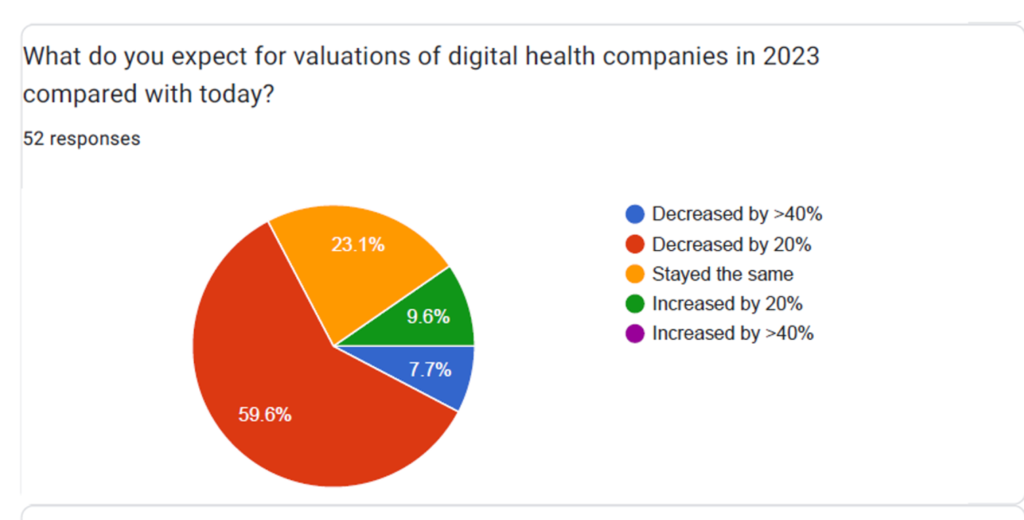

Most of the 50+ responses to the survey expect that in 2023, valuations for digital health companies will decrease by over 20%: that’s a net of 83% including 60% expecting valuations to fall 20-40%, and 23% anticipating declines of over 40% of valuations in the next year.

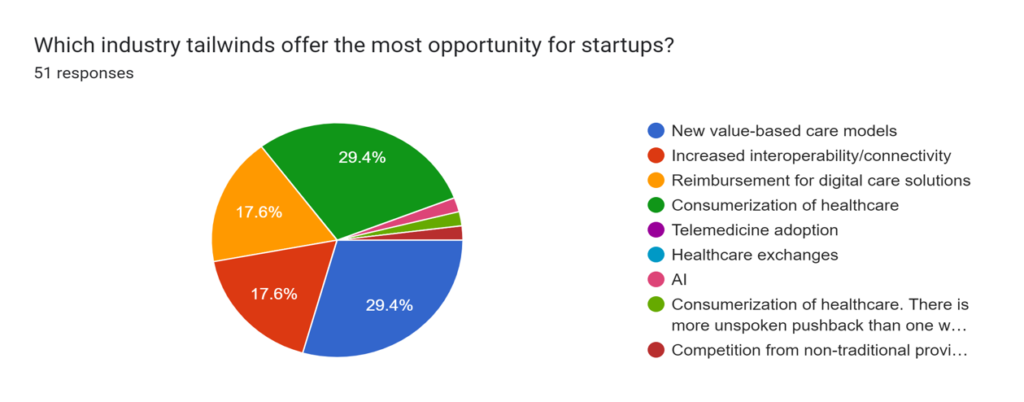

On the upside, digital health investors see greatest opportunity for start-ups to focus on value-based care models and consumerization of healthcare businesses (each with 29% of investors keen), followed by interoperability and connectivity and reimbursement for digital health solutions (with over 17% enthusiastic for each).

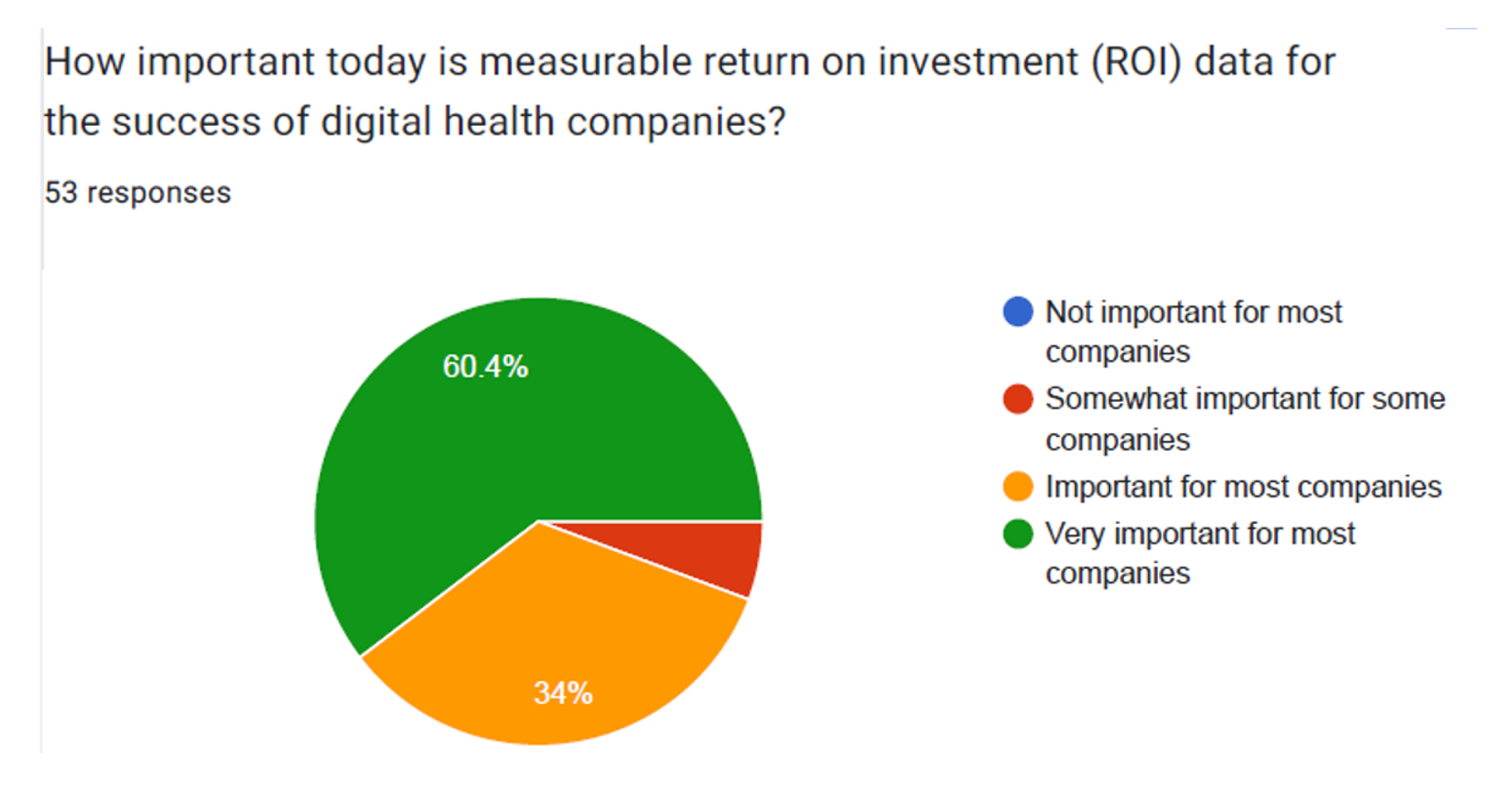

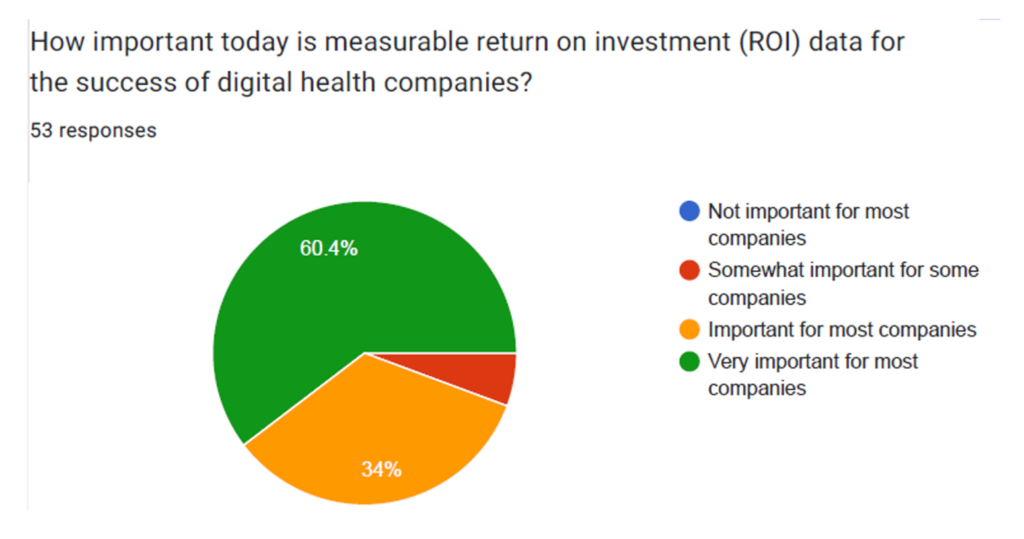

Regardless of the clinical area or solution a digital health start-up is addressing, investors are saying “show me the money and the ROI” for that venture: Virtually all of the investors studied told GSR that a measurable teturn on investment would be important or very important for most companies.

Furthermore, 8 in 10 investors said that clinical evidence and trials backing up the innovations would be important or very important.

The investors also ranked sectors holding the most promise in digital health for 2023; these are expected to be:

- AI/machine learning (45%)

- Healthcare data and analytics (37%)

- Remote patient monitoring (29%)

- AI drug discovery and clinical trial technology (each at 27%), and,

- Interoperability (22%).

Key clinical spaces holding the most promise, investors said, were oncology, mental health, primary care, and neurology.

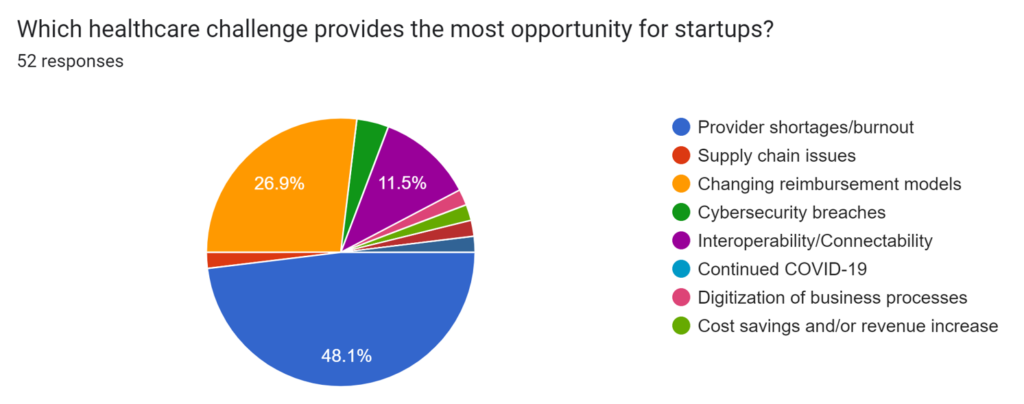

Health Populi’s Hot Points: It’s good to see the investors’ focusing in on digital health solutions and investment opportunities to address provider shortages and clinician burnout: roughly one-half of the investors called out burnout and shortages, which compromises a key pillar in the Quadruple Aim: the wellbeing of the clinical workforce.

The second most prominent health care challenge presenting investment opportunities for digital health was changing reimbursement models, which another part of the survey related to value-based payment. This area, too, can help address and solve for fragmentation of services, aligning the value and values of both clinicians and patients alike.

Looking to 2023, the clinical evidence and ROI that support clinicians’ wellbeing and value-based care, together, could drive returns-on-investments across several dimensions: for health systems and larger health economies, as well as for individual clinicians’ and patients’ wellbeing and outcomes.

I'm gratified to be named on

I'm gratified to be named on  I’m celebrating America’s 250th birthday both patriotically and professionally, honored that the NLM included my 2010 paper, “How Smartphones Are Changing Healthcare for Consumers and Patients” as one of 250 items curated for the digital archive of 250 Years of American Medicine.

I’m celebrating America’s 250th birthday both patriotically and professionally, honored that the NLM included my 2010 paper, “How Smartphones Are Changing Healthcare for Consumers and Patients” as one of 250 items curated for the digital archive of 250 Years of American Medicine.