In the growing era of consumer-driven health, a growing list of options for receiving care are available to consumers. And people are liking new-new sites of care that are more convenient, cheaper, price-transparent, and digitally-enabled.

In the growing era of consumer-driven health, a growing list of options for receiving care are available to consumers. And people are liking new-new sites of care that are more convenient, cheaper, price-transparent, and digitally-enabled.

Think of these new-new sites as “new front doors,” according to Oliver Wyman in their report, The New Front Door to Healthcare is Here.

The traditional “doors” to primary and urgent care have been the doctor’s office, hospital ambulatory clinics, and the emergency room. Today, the growing locations for retail clinics and urgent care centers are giving consumers more visible and convenient choices for seeking care.

And one other locale is gaining traction: virtual care in the patient’s home or workplace via digitally-enabled platforms. THINK: Skype-meets-Dr. Kildare or Dr. McDreamy (or pick your favorite doctor).

So “the new front door” isn’t really a door: it’s a well-designed, nice-to-use, venue for health and health care. Based on Oliver Wyman’s consumer survey, those new doors are gaining traction with new healthcare consumers. Both familiarity with the concepts and use of them are growing: for example,

- 15% of consumers used retail clinics in 2013, and 26% did so in 2015

- 8% of consumers used remote or virtual consultations in 2013, and 12% did in 2015.

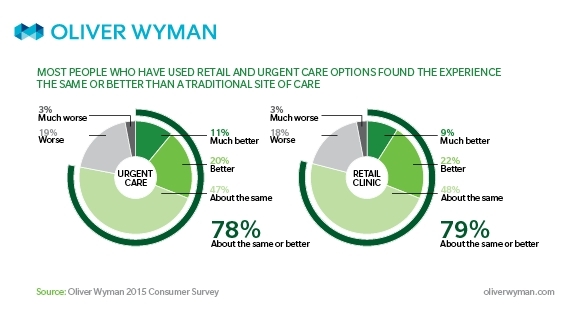

Note that consumers with “new front door” healthcare experiences are less willing to use a traditional doctor’s office again, the study learned. That’s probably because about 8 in 10 consumers who used either urgent care or a retail clinic said they received about the same or better care experience as in a traditional healthcare setting.

Certain conditions would motivate a consumer to use a health and wellness clinic in a retail setting:

- 42% would use it only if their health plan covered some or all of the cost

- 32% would use it only if were affiliated with a local hospital, provider, or their own doctor

- 21% would use it if they could afford it.

Only 17% would “never” use this new door for healthcare.

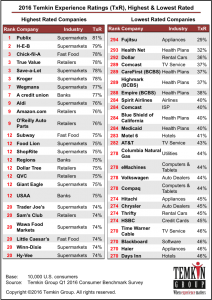

Health Populi’s Hot Points: As patients continue to morph into health consumers learning to use high-deductible health plans and HSAs, they seek retail-style service and products for in the health ecosystem that match up with other retail segments in their lives. Check out the 2016 Temkin Group Insight Report on consumers’ experience ratings by industry.

Health Populi’s Hot Points: As patients continue to morph into health consumers learning to use high-deductible health plans and HSAs, they seek retail-style service and products for in the health ecosystem that match up with other retail segments in their lives. Check out the 2016 Temkin Group Insight Report on consumers’ experience ratings by industry.

Consumers rank supermarket chains at the top of their experience list, followed by fast food chains, retailers, parcel delivery services, and banks.

At the low end? Internet service providers, TV service providers, and health plans.

Until health care can design itself with true consumer-centered principles (including and beyond the person’s “patient”-persona), traditional players will see the start of consumer health migration to retail settings for low-hanging (and profitable) health-and-wellness fruit.

One of the best aspects of my work is collaborating across the health/care ecosystem to address how health citizens can deal with health care costs and and care for families. I'm grateful to have collaborated with Fidelity on their research into this issue,

One of the best aspects of my work is collaborating across the health/care ecosystem to address how health citizens can deal with health care costs and and care for families. I'm grateful to have collaborated with Fidelity on their research into this issue,  I'm gratified to be named on

I'm gratified to be named on  I’m celebrating America’s 250th birthday both patriotically and professionally, honored that the NLM included my 2010 paper, “How Smartphones Are Changing Healthcare for Consumers and Patients” as one of 250 items curated for the digital archive of 250 Years of American Medicine.

I’m celebrating America’s 250th birthday both patriotically and professionally, honored that the NLM included my 2010 paper, “How Smartphones Are Changing Healthcare for Consumers and Patients” as one of 250 items curated for the digital archive of 250 Years of American Medicine.