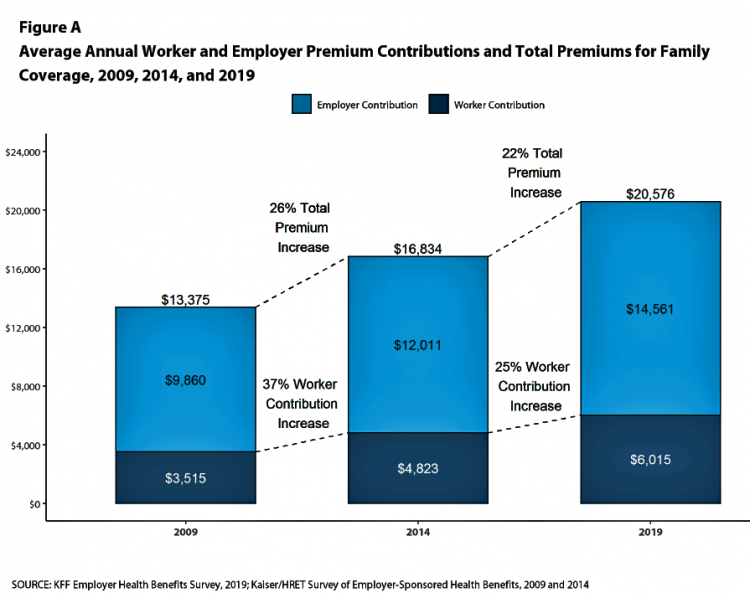

Here’s the latest arithmetic on American workers’ financial trade-off of wages for health care insurance coverage: in the ten years since 2009, family premiums have risen 54% and workers’ contribution to health care spending grew 71%. Wages? They rose 26%, and general price inflation by 20%, according to the Kaiser Family Foundation survey on employer-sponsored benefits for 2019 released yesterday.

Survey details for this 21st annual encyclopedia on employer-sponsored health care are published in Health Affairs October 2019 issue in a paper titled, Health Benefits in 2019: Premiums Inch Higher, Employers Respond to Federal Policy.

Because this is the Health Populi blog, my lens is aimed in the KFF report on consumer-facing issues. In his remarks during a press call yesterday, Drew Altman, KFF President and CEO, said that American workers’ current perspective on health care is “cost versus coverage.”

In 2019, ”cost” for health consumers translates into the premium, deductible, out-of-pocket spending, and surprise medical bills — an issue that’s getting a lot of attention in U.S. politics both at the Federal and State levels.

Overall, 57% of employers offer health benefits — equal to offer levels in 2018 and similar to the 2009 level of 59%. Larger companies are more likely to offer health insurance to workers than smaller companies. [Note that it’s small companies where new jobs are likely to be created in the U.S. economy]. Workers in lower-wage firms are less likely to be offered health benefits, as well — and those firms offer insurance at higher premiums than larger, better-paying companies do. This results in fewer workers in lower-wage firms taking advantage of opting in to health benefits: 33% workers in lower-wage firms are covered by their company’s health plans, compared with 63% of workers in other companies.

The third chart illustrates various health benefits offered by employers in 2019, most prevalent of which are telehealth (offered by 90% of large companies and 69% of all companies with at least 50 workers), and coverage for retail clinic visits, extended by over 8 in 10 companies offering health benefits.

On-site clinics and high performance networks are offered by about one-third of larger companies.

Employer health plans also continue to offer wellness programs to workers, including health risk assessments and biometric screenings, coupled with incentives to behaviorally “nudge” employees to participate. KFF also gauged employers’ using wearable devices in wellness programs: 18% of large companies offering health benefits collected information from workers through mobile apps or wearable tech, and 10% of the big firms provided the wearable tech as part of a health improvement program.

Health Populi’s Hot Points: KFF concludes the Health Affairs analysis asserting that, “As in 2018, there were no big changes in the market for employer-sponsored coverage in 2019…Given this relative stability in premium growth and coverage, the vibrant public debate about whether the U.S. needs a public insurance program to replace or be an alternative to private coverage might come as a surprise.”

The essay continues: “One reason may be the widespread concerns about affordability voiced by people in employer-based plans.”

Indeed, it seems that in the eyes of health consumers, “It’s the deductible, stupid.”

Deductibles exceed the asset base that “many of those with private” sector health coverage have managed to save, KFF noted in a study published in 2017 succinctly titled, “Do health plan enrollees have enough only to pay cost sharing?”

The answer is surely, “no,” Americans don’t, which is the basis for the first chapter of my book, HealthConsuming, describing “The Patient Is the Payor.”

The latest data on Americans’ savings show an uptick in saving, prompting top-line observers to say, “good job.” But lifting the hood up on this statistic shows that it’s consumers at the highest income levels who have been saving, and credit/borrowing is growing among people at lower income levels.

Expect health care costs to rank a top issue driving U.S. voters to polls in 2020, and for the call for some form of universal health care to continue — all due to the financial health care cost risk-shift to Americans at work and in retirement.

I'm gratified to be named on

I'm gratified to be named on  I’m celebrating America’s 250th birthday both patriotically and professionally, honored that the NLM included my 2010 paper, “How Smartphones Are Changing Healthcare for Consumers and Patients” as one of 250 items curated for the digital archive of 250 Years of American Medicine.

I’m celebrating America’s 250th birthday both patriotically and professionally, honored that the NLM included my 2010 paper, “How Smartphones Are Changing Healthcare for Consumers and Patients” as one of 250 items curated for the digital archive of 250 Years of American Medicine.