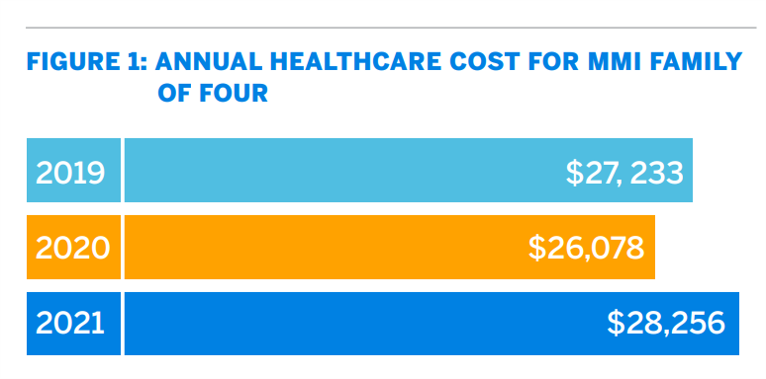

The good news for health care costs for a family of four in America is that they fell, for the first time in like, ever, in 2020.

But like a déjà vu all over again, annual health care costs for a family of four enrolled in a PPO will climb to over $28,000 in 2021, based on the latest 2021 Milliman Medical Index (MMI).

The first chart shows how health care costs declined in our Year of COVID, 2020, by over $1,000 for that hypothetical U.S. family. But costs rise with a statistical vengeance this year, by nearly $2,200 per family–about 8.4% higher over the year.

That 8.4% is higher than historical cost increases in the MMI seen in the past five years.

What caused costs to decline in 2020 were “eliminated and deferred care,” the Milliman analysts write, which offset the direct costs of COVID-19 testing and treatment. All categories of health care costs were lower in 2020 versus 2019, with the exception of prescription drugs.

Milliman’s human capital experts include actuaries, who were transparent in last year’s MMI published in May 2020 to say that there were many uncertainties in that forecast. We humbly recall, collectively, we didn’t know what we didn’t know at the time about the costs of caring for coronavirus patients, the eventual tragic mortality rate in the U.S., and how much care would be postponed or never realized in the health care system.

Milliman’s human capital experts include actuaries, who were transparent in last year’s MMI published in May 2020 to say that there were many uncertainties in that forecast. We humbly recall, collectively, we didn’t know what we didn’t know at the time about the costs of caring for coronavirus patients, the eventual tragic mortality rate in the U.S., and how much care would be postponed or never realized in the health care system.

A big uncertainty in this year’s forecast, pondering the 2022 picture, is what extent eliminate care will have on future adverse health outcomes….something that keeps my scenario planning humming across various modeling.

A big uncertainty in this year’s forecast, pondering the 2022 picture, is what extent eliminate care will have on future adverse health outcomes….something that keeps my scenario planning humming across various modeling.

Other uncertainties address changing health care workflows, asking the question of how much virtual care will persist in 2021 and beyond, along with growing demand for mail order pharmacy use.

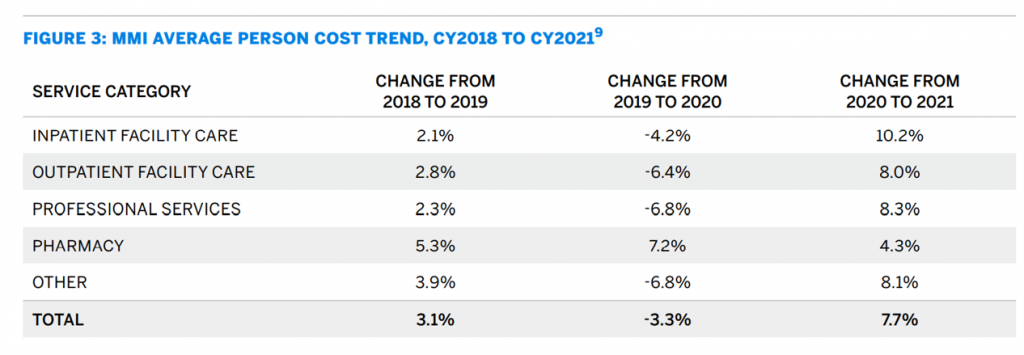

Looking at Figure 3, the table on average person cost trends to 2021, we see that costs grow for every service category in 2021. These increases range from the highest percentage change for inpatient care, over 10%, followed by professional services (e.g., physician office visits) growing by 8.3%, and outpatient facility care expanding by 8.0% cost-wise. Pharmacy costs are expected to grow more slowly, at 4.3% up, compared with the largest cost increase across categories in 2020 of 7.2%. Milliman points out that in the 2020 pandemic, utilization reductions seen in other health care components did not impact prescription drugs in the same way.

While there is no “typical” family of four, Milliman has used the 4-person construct for many years so we can compare annual changes based on that scenario.

While there is no “typical” family of four, Milliman has used the 4-person construct for many years so we can compare annual changes based on that scenario.

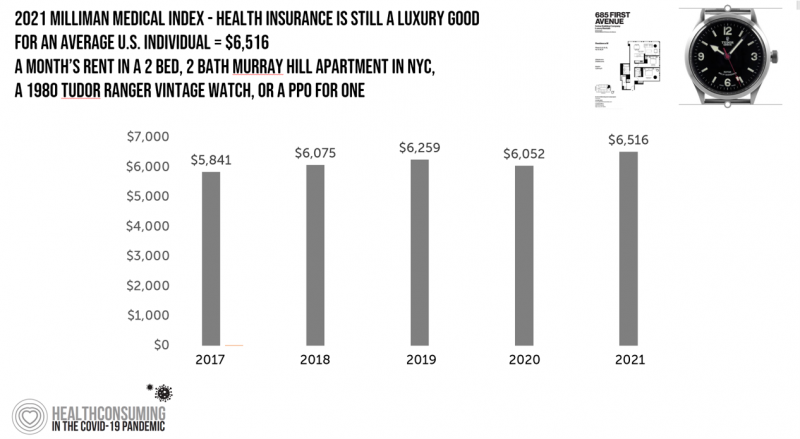

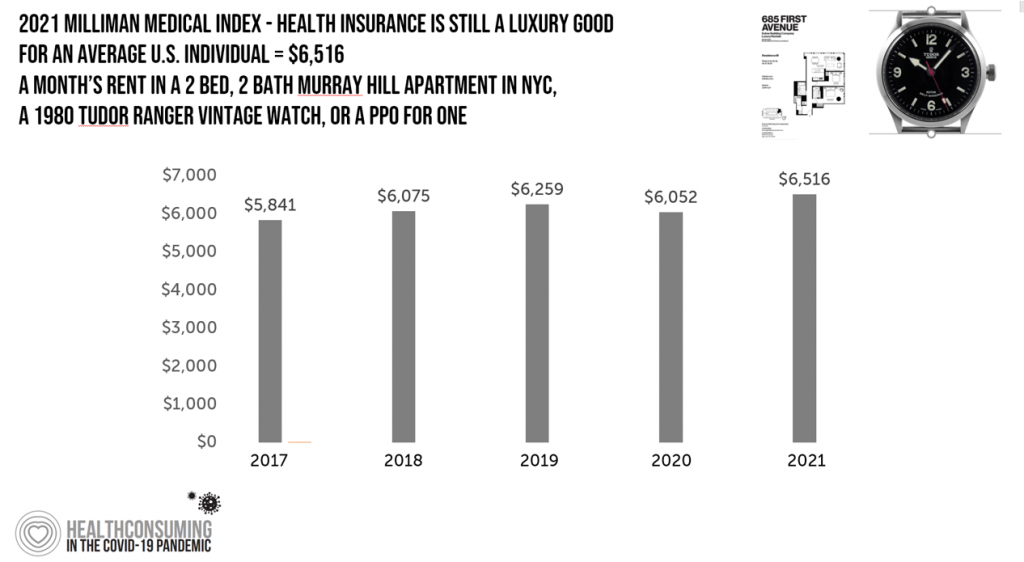

The team also calculated annual health care costs per individual, which are expected to be $6,516 in 2021, about 7.6% higher than in 2020.

Each year, I figure out what the average PPO cost could buy someone in exchange for that health insurance. This year, I assert that health coverage is a luxury good, equivalent at $6500 to a month’s rent in a luxe renovated apartment in Murray Hill NYC in an amenity-rich high-rise, or a vintage 1980 Tudor Ranger watch.

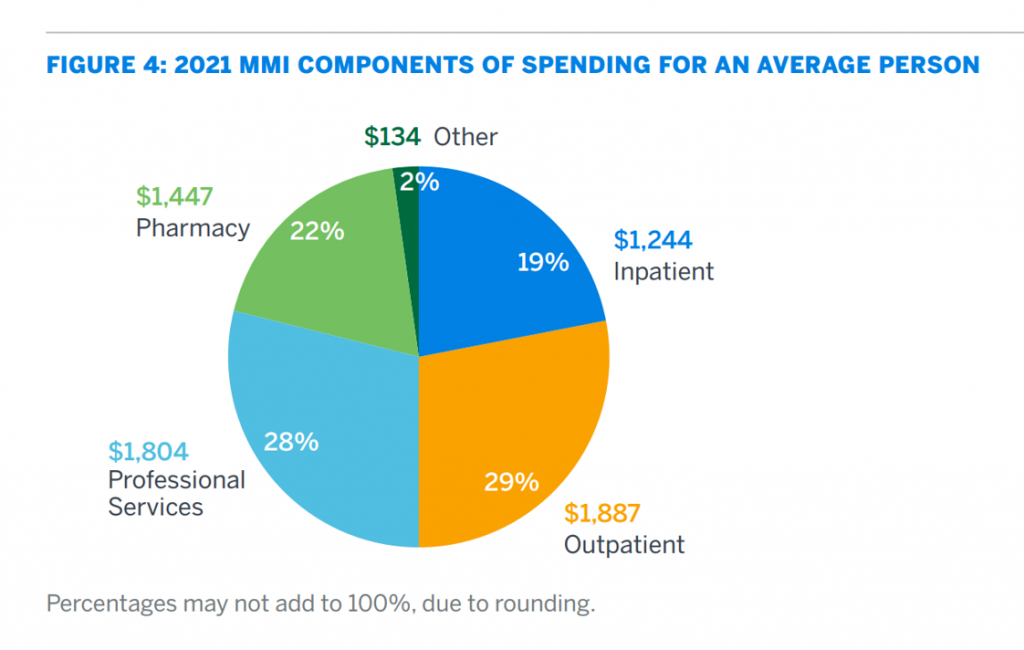

The pie chart shown in Figure 4, breaks out an individual person’s health care costs by component, with outpatient and professional services roughly equal at just over one-quarter of spending each. Nearly hitting that mark are pharmacy costs, now reaching 22% of the individual health care spending. Finally, inpatient costs compris0e about $1 in every $5, just below pharmacy spending.

You can read four years of my previous takes on the MMI here on Health Populi at these links…

Health Populi’s Hot Points: A key data point I focus on each year is the proportion of health care costs borne by the employee of the company compared with the cost burden for her employer.

Health Populi’s Hot Points: A key data point I focus on each year is the proportion of health care costs borne by the employee of the company compared with the cost burden for her employer.

In 2021, that piece of the health care cost pie is 42%, comprising $1,711 for the worker’s contribution to a health plan, and $1,066 in out-of-pocket costs. (Remember, this is average cost for the average single person; some workers covered at work will spend more, and some will spend less).

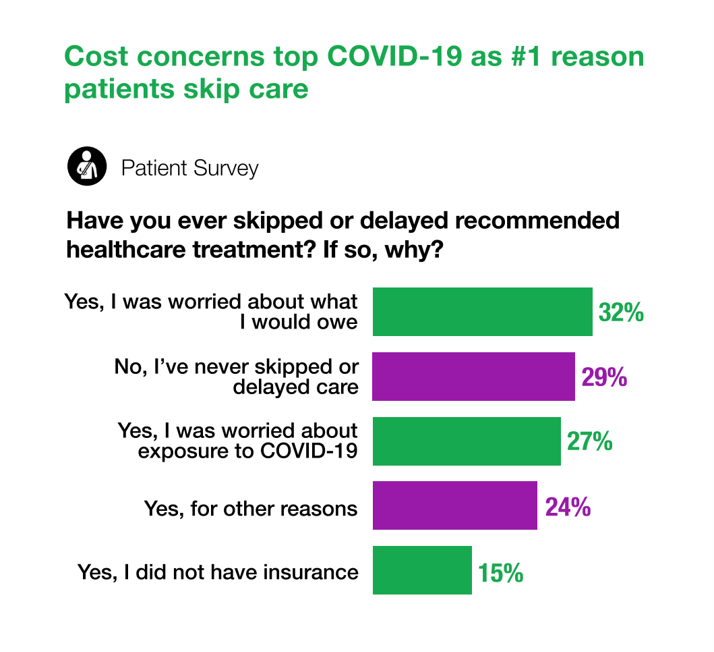

Health care spending is a household budget issue, with costs competing and/or crowding out other consumer spending. According to the newly-published Patientco 2021 State of the Patient Financial Experience Report, one of the top 3 reasons patients cancelled health care visits is worry about cost (among 41% of U.S. consumers).

In fact, cost concerns top COVID-19 as the #1 reason patients currently skip care, Patientco found in its consumer survey.

Avoiding health care due to cost is more common among women (34%) than men (30%), keeping in mind that a greater proportion of women were negatively impacted by pandemic economics and unemployment than men in the U.S.

For patients under 60 years of age, 41% skipped care because they were concerned about what they would owe compared with 30% skipping care due to COVID-19 concerns.

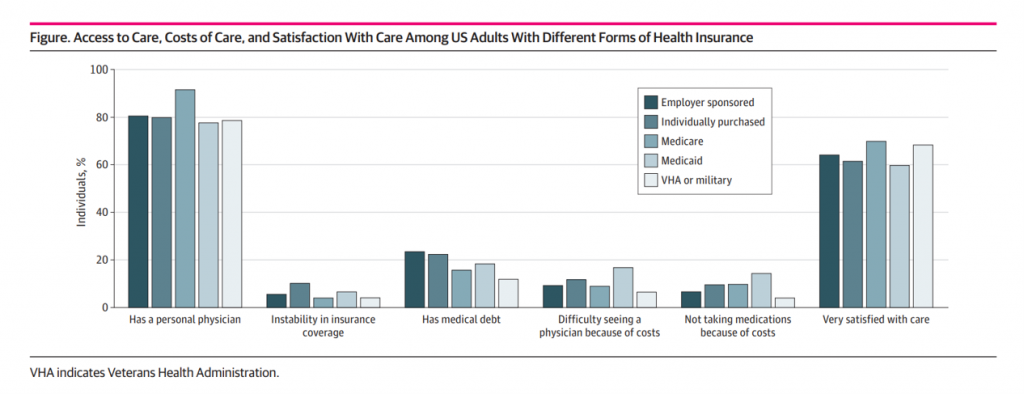

Coupled with these findings from Patientco (which recently won the “Best in KLAS” award for patient financial engagement platforms), an article in JAMA Network Open published this week (dated June 1, 2021) looks at access to care, cost of care, and satisfaction with care among adults with private and public health insurance in the U.S.

Coupled with these findings from Patientco (which recently won the “Best in KLAS” award for patient financial engagement platforms), an article in JAMA Network Open published this week (dated June 1, 2021) looks at access to care, cost of care, and satisfaction with care among adults with private and public health insurance in the U.S.

This study analyzed the data from 149,290 U.S. adults living in 17 States and DC who had one of five types of health care coverage, public and private.

The study found that people who had purchased private insurance were more likely to report poor access to health care, higher costs of care, and less satisfaction with care versus people covered by publicly sponsored health insurance plans.

As the last chart from the JAMA study illustrates, patients covered by employer sponsored care tended to land on the higher side of having medical debt. At the same time, they were not as satisfied with their health care as people enrolled in Medicare or a VA/military health plan.

The Milliman actuaries are right to cite many uncertainties that will shape health care utilization, costs, and spending in 2021. Another wild card to throw into this mix is the likelihood that employers will want to continue to be in the health insurance game in the post-pandemic economy, and how financial health for millions of American workers (especially women) will shake out in the 2022 version of the Milliman Medical Index.

I'm gratified to be named on

I'm gratified to be named on  I’m celebrating America’s 250th birthday both patriotically and professionally, honored that the NLM included my 2010 paper, “How Smartphones Are Changing Healthcare for Consumers and Patients” as one of 250 items curated for the digital archive of 250 Years of American Medicine.

I’m celebrating America’s 250th birthday both patriotically and professionally, honored that the NLM included my 2010 paper, “How Smartphones Are Changing Healthcare for Consumers and Patients” as one of 250 items curated for the digital archive of 250 Years of American Medicine.