Rising costs, generational shifts, digital transformation, and fast-growing investments in new health care models and technologies are forcing change in the legacy health care, noted in the State of Consumerism in Healthcare 2021: Regaining Momentum, from Kaufman, Hall & Associates.

As the title of Kaufman Hall’s sixth annual report suggests, health care consumers are evolving — even if the traditional healthcare system hasn’t uniformly responded in lock step with more demanding patients.

Kaufman Hall analyzed 100 health care organizations in this year’s consumerism survey to assess their readiness to embrace consumer-centric strategies, understand how the industry prioritizes these approaches, evaluate their progress toward responding to them, and identifying best practices.

Kaufman Hall analyzed 100 health care organizations in this year’s consumerism survey to assess their readiness to embrace consumer-centric strategies, understand how the industry prioritizes these approaches, evaluate their progress toward responding to them, and identifying best practices.

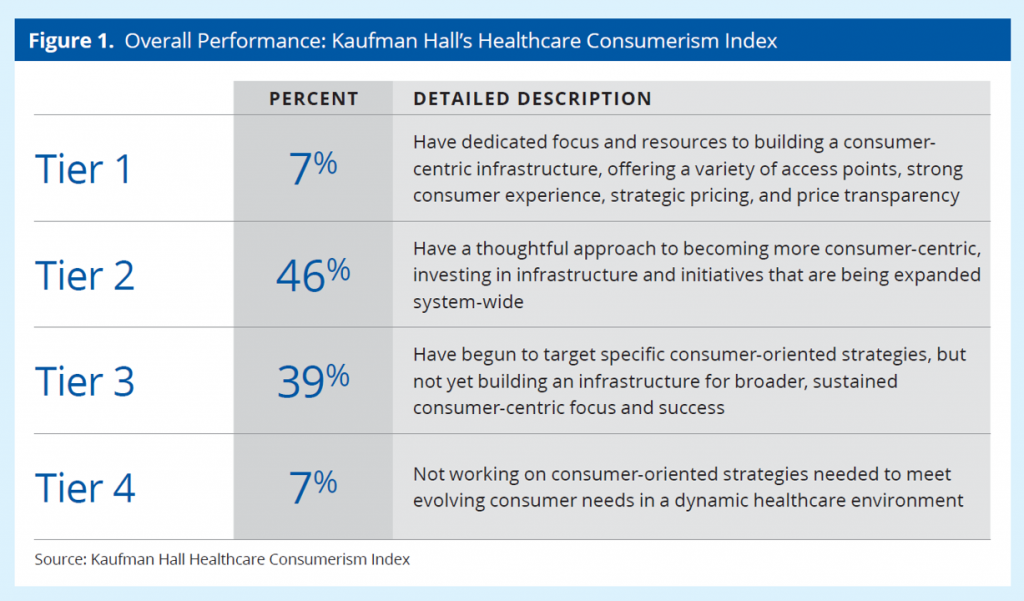

The firm has tracked healthcare providers’ embrace of health consumers over the years, segmenting the industry into four tiers as shown in the first chart: from Tier 1, with a dedicated focus and resources allocated to address health consumers at the strategic center, to Tier 4, the lowest level of effort and resources devoted to consumer-oriented strategies.

In 2021, nearly one-half of hospitals and health systems ranked in Tier 2, with in Kaufman Hall’s words, “a thoughtful approach to becoming more consumer centric,” investing in digital infrastructure and programs across the enterprise. Another 4 in 10 providers were in Tier 3, beginning to target specific consumer health strategic, but not across the enterprise in a sustained way. The remaining 14% of providers fall into the outer tiers, 1 and 4, firmly focused on consumers at the center, or not working much on health consumers in their strategies.

The COVID-19 pandemic moved consumers to undergo personal digital transformation when they could do so — for work, for school, for faith-activities, for fitness, for fun and socialization. [The limiting factor for this was access to connectivity, as broadband became increasingly recognized as a social determinant for health and daily living].

The COVID-19 pandemic moved consumers to undergo personal digital transformation when they could do so — for work, for school, for faith-activities, for fitness, for fun and socialization. [The limiting factor for this was access to connectivity, as broadband became increasingly recognized as a social determinant for health and daily living].

As patients have continued to morph into health consumers, they expect more digital access and convenience from their health care touchpoints and experiences. This observation has not gone unnoticed by both new entrants and existing industry stakeholders such as health plans and pharmacies, many of which have added health care to their core businesses or have been vertically integrating their health care portfolios.

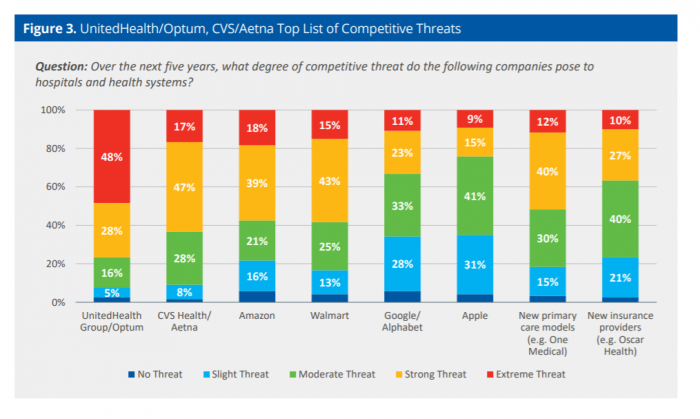

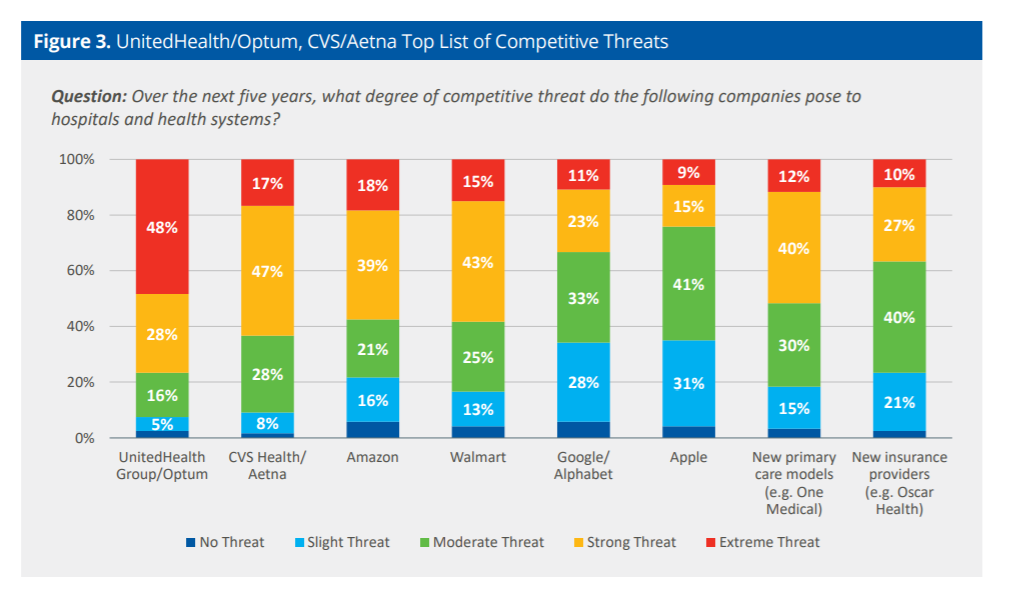

The second bar chart (labeled Figure 3) illustrates some of the most competitive threats Kaufman Hall’s research identified. The most visible threat was seen from UnitedHealth Group, with 3 in 4 hospitals noting UHG as a formidable threat to their health system business. CVS Health/Aetna, Amazon, and Walmart rank in the next-most competitive group impacting hospitals, followed by new primary care models.

That digital convenience enables another feature the new health consumer expects, especially accelerated during the pandemic: omni-channel health care services, delivered where a person wants to “consume” or receive that care — at home, in one’s hands via a mobile phone or laptop computer, closer to home in a pharmacy or community health place, at school, in a grocery store, or gym.

That digital convenience enables another feature the new health consumer expects, especially accelerated during the pandemic: omni-channel health care services, delivered where a person wants to “consume” or receive that care — at home, in one’s hands via a mobile phone or laptop computer, closer to home in a pharmacy or community health place, at school, in a grocery store, or gym.

And of course, in their favored brick-and-mortar hospital, ambulatory care center, clinic, or doctor’s office.

Those legacy health care providers showed humility in the Kaufman Hall report with most noting the need to re-design and expand digital and physical facilities responding to the COVID-19 pandemic, as well as implementing innovative care models — but many confessing they do not currently provide best-in-class responses to these high priorities.

Health Populi’s Hot Points: “The pandemic really upended our plans, which is actually a good thing,” one respondent told Kaufman Hall. “We weren’t bold enough in our thinking.”

Health Populi’s Hot Points: “The pandemic really upended our plans, which is actually a good thing,” one respondent told Kaufman Hall. “We weren’t bold enough in our thinking.”

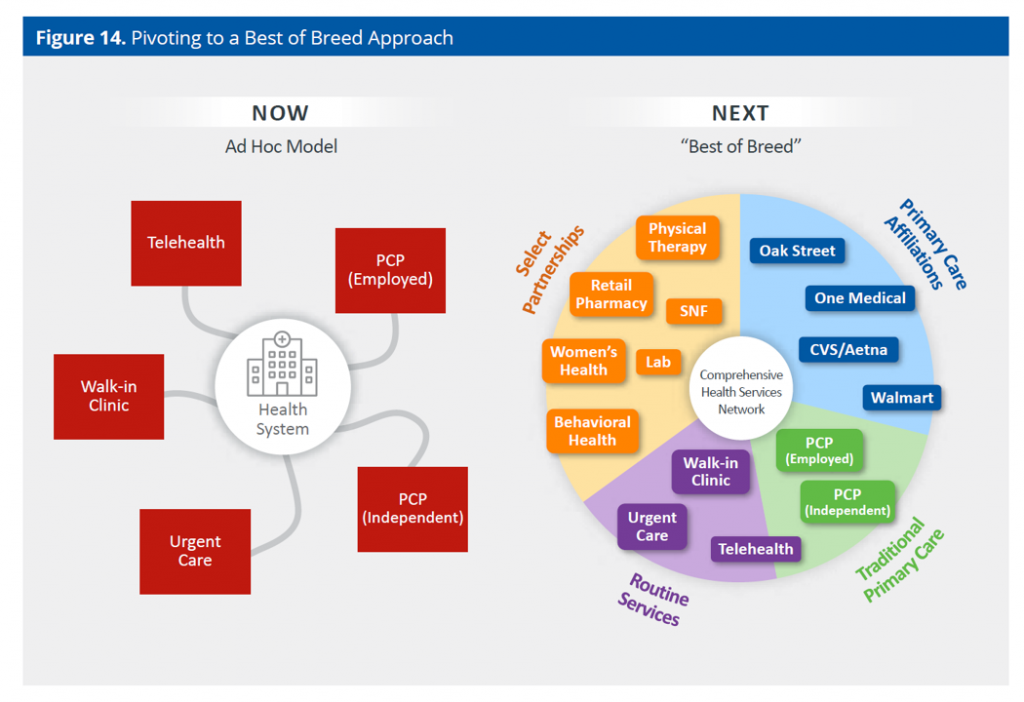

This last graphic from the report summarizes Kaufman Hall’s view on the visible, possible future of “best of breed” health care, re-imagining the current model of what they term ad hoc care.

The central thesis of the best of breed care vision is networked, comprehensive health services across a continuum, from routine services to “traditional” primary care via PCPs, primary care affiliations with new-fangled organizations such as Oak Street and One Medical, and partnerships that can be crafted with many key services for women’s health, men’s health, lab services, mental and behavioral health, and other specialty and ancillary areas.

A new report from UPMC and KLAS further confirms the moving target of health care incumbents adding telehealth and investing in digitalization for traditional brick-and-mortar delivery sites. The report’s title underscores the driving force: The Intersection of Value and Telehealth.

That value could be accomplished through a fierce focus on chronic care integrating primary care and behavioral/mental health, making broadband access universal and accessible, and deploying digital front doors that people can access based on value and their values.

Thank you

Thank you  Jane joined host Dr. Geeta "Dr. G" Nayyar and colleagues to brainstorm the value of vaccines for public and individual health in this challenging environment for health literacy, health politics, and health citizen grievance.

Jane joined host Dr. Geeta "Dr. G" Nayyar and colleagues to brainstorm the value of vaccines for public and individual health in this challenging environment for health literacy, health politics, and health citizen grievance.