As more than 1 in 3 U.S. workers were unemployed during the pandemic and another 38% had reductions in hours and pay, Americans’ personal forecasts and expectations for retirement have been disrupted and dislocated.

![]()

In its look at The Road Ahead: Addressing Pandemic-Related Setbacks and Strengthening the U.S. Retirement System from the Tramsamerica Center for Retirement Studies (TCRS), we learn about the changing views of U.S. workers on their future work, income, savings, dreams and fears.

Since 1988, TCRS has assessed workers’ perspectives on their futures, this year segmented the 10,003 adults 18 and over in 3 groups: employed workers, self-employed workers, and people who were unemployed but looking for work. The study was fielded between October and December 2021, thus before the onset of significant inflation on household budgets in 2022.

While most employed workers have been saving for retirement, many are not putting sufficient funds away for their goals, dreaming of traveling, spending more time with family, and pursuing hobbies. A substantial (“concerning” in the words of TCRS) 3 in 5 employed workers have taken an early or hardship withdrawal from their retirement accounts; key reasons for taking retirement money out of a 401(k) pre-retirement were paying off credit card debt, every day expenses, for financial emergencies, home improvements, or for medical bills (among 23% of those making early withdrawals).

For the self-employed, the pandemic has been more challenging for retirement savings, with 35% finding themselves unemployed at some point in the pandemic. This is an optimistic group that envisions long, financially productive lives without an expectation to retire young. Interestingly, 85% of self-employed people who intend to work at least part-time in later years would do so for healthy-aging reasons and not as much for financial gain.

![]()

Most workers made financial adjustments during the pandemic, most notably by reducing daily expenses (for groceries and telecomms, among other line items), dipping into savings accounts, accumulating new credit card debt, and borrowing money from other people (most likely among people who were unemployed by a factor of nearly 2 to 1).

15% of workers delayed or avoided health care as a financial adjustment to the family budget in the pandemic.

![]()

We know that behavior change for health is challenging even without dealing with pandemic stress. TCRS assessed workers’ engagement in healthy activities, finding that employed people were more likely to eat healthier (especially self-employed folks) vs. unemployed people. Regular exercise was also more prominent among working people compared with those not working. And workers (whether self-employed or otherwise) were more likely to take COVID-19 precautions such as wearing a mask, physically distancing, and hand hygiene vs. the unemployed group int he study.

With the exceptions of managing stress and socializing with family and friends remotely, those were who unemployed were less likely to undertake any of the healthy activities analyzed by TCRS.

![]()

Health Populi’s Hot Points: One of the most valuable insights the TCRS study considers is its looking into “Happiness and Health,” assessing peoples’ retirement dreams as well as retirement fears.

As mental health converges so intimately with physical health and financial health, this part of the study is so important (and appreciated!).

This last chart organizes the Retirement Dreams data overall and by the 3 worker segments in the study. The granular findings are important, noting differences across the three groups:

- For the unemployed folks, one-in-four do not have “any” retirement dreams (the bar on the far right of the chart)

- For self-employed people, the most outlying statistic is for continuing to work int he same field, over 50% more likely to be planned compared with those who are employed by a company

- For those employed (not self-), the high bar is for spending time with family and friends and pursuing hobbies — thus, more leisure time expected among this group of workers.

Across all people in this study, the bottom-line for us to consider — sobering, to be sure — is for savings.

![]()

In the report’s section on “Retirement Savings, Planning, and Preparation,” we learn that the median household retirement savings across all workers was $54.000 as of late 2021. This ranged from $65,000 for employed workers to $42,000 for self-employed people and $200 for those who were unemployed.

People expressed their estimated retirement savings needs as,

- $350,000 among the total workforce, segmented by,

- $400,000 for those who were employed,

- $500,000 for the self-employed group, and

- $100,000 for the unemployed.

How did people calculate those estimate retirement savings amounts?

Overall, 45% of people “guessed,” led by 61% of those who were unemployed.

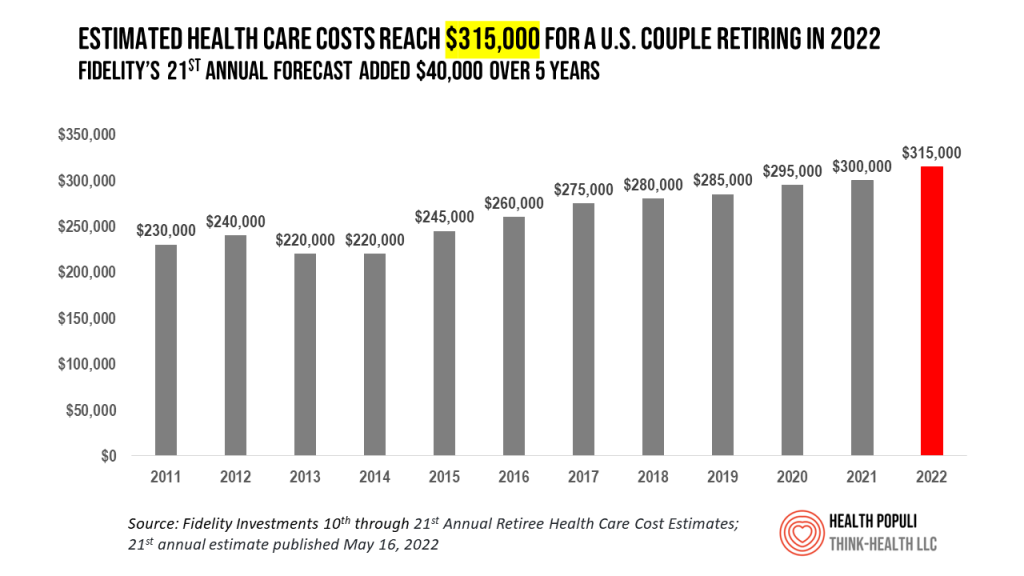

With that context, I’ll leave you with the latest estimate from Fidelity Investments on how much money a couple retiring in 2022 at 65 years of age would need to cover their health care costs in retirement — just their medical costs, not living or traveling or other expenses — and not including long-term care.

That big nut would be $315,000.

So much for Savings, Planning, and Preparation.

And what was that the TCRS survey said about managing stress?

Thank you

Thank you  Jane joined host Dr. Geeta "Dr. G" Nayyar and colleagues to brainstorm the value of vaccines for public and individual health in this challenging environment for health literacy, health politics, and health citizen grievance.

Jane joined host Dr. Geeta "Dr. G" Nayyar and colleagues to brainstorm the value of vaccines for public and individual health in this challenging environment for health literacy, health politics, and health citizen grievance.