When you think about life insurance, images of actuaries churning numbers to construct mortality tables may come to mind. Mortality tables show peoples’ life expectancy based on various demographic characteristics.

When you think about life insurance, images of actuaries churning numbers to construct mortality tables may come to mind. Mortality tables show peoples’ life expectancy based on various demographic characteristics.

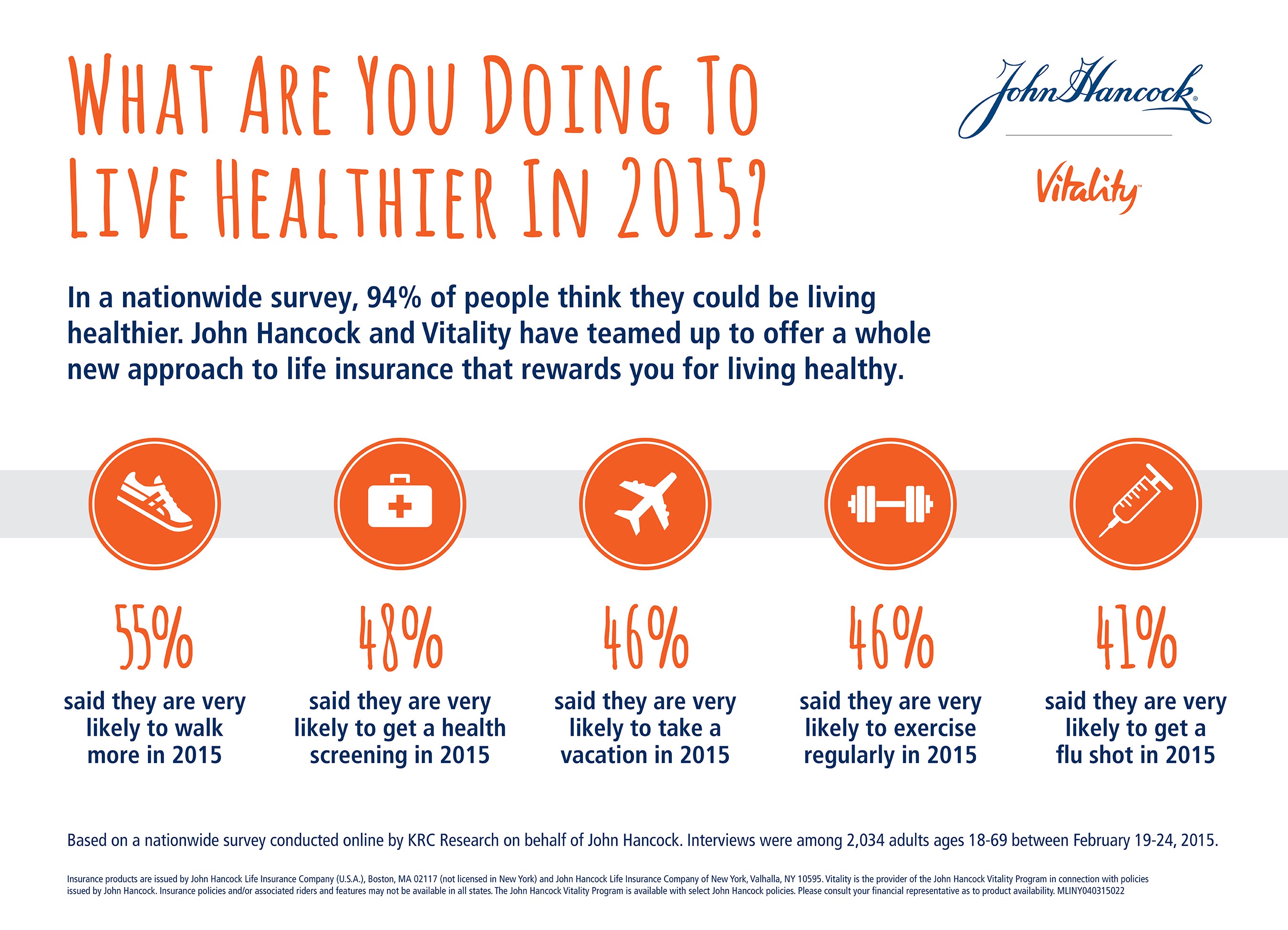

John Hancock is flipping the idea life insurance to shift it a bit in favor of “life” itself. The company is teaming with Vitality, a long-time provider of wellness tools programs, to create insurance products that incorporate discounts for healthy living. The programs also require people to share their data with the companies to quality for the discounts, which the project’s press release says could amount to $25,000 over the course of a life of a couple buying insurance at 45 for a benefit of $500,000, assuming the couple live to 85.

Participating in various activities in the program will earn policyholders Vitality Points, which can result in as much as a 15% discount on the life insurance premium each year.

While this tactic is relatively new to the life insurance fold, many automobile insurance companies already provide discounts based on personal drivers’ behaviors.

Health Populi’s Hot Points: Through the consumer/retail health lens, what’s promising about John Hancock’s program is bringing the idea of health and wellness to the traditional dullsville of life insurance. How to make the purchase of life insurance more engaging, I daresay even fun? By talking about the health benefit, versus the death benefit.

While it’s still early days regarding peoples’ engagement with wearable devices for health over the long, sustainable run, John Hancock’s plan will be worth watching from that point-of-view.

On the personal data-sharing front, this will be a case study to observe and learn from, as well. How keen will people be to trade off their metrics and personal health data on lifestyle and exercise, vis-a-vis the level of premium discount on offer? This is an experiment in behavioral/health economics.

When it comes to privacy and how John Hancock will use the data, they’ll need to be up-front, transparent and clear about how the data will be used and where it will be traveling outside of John Hancock and Vitality’s data clouds.

And remember, nothing is stopping consumers enrolling in this plan from sharing their thoughts and experiences on social networks, which could impact the John Hancock brand in positive and not-so-great ways.

Remember, too, that life insurance companies’ brand equity is down there with pharma, financial services and airlines. Who’s on top? Technology, travel and tourism, consumer goods and retail. John Hancock’s reimagination of life insurance bundled with wellness could up-tier the firm’s brand equity toward the more beloved consumer/retail segment. Watch this space.

Interviewed live on BNN Bloomberg (Canada) on the market for GLP-1 drugs for weight loss and their impact on both the health care system and consumer goods and services -- notably, food, nutrition, retail health, gyms, and other sectors.

Interviewed live on BNN Bloomberg (Canada) on the market for GLP-1 drugs for weight loss and their impact on both the health care system and consumer goods and services -- notably, food, nutrition, retail health, gyms, and other sectors. Thank you, Feedspot, for

Thank you, Feedspot, for  As you may know, I have been splitting work- and living-time between the U.S. and the E.U., most recently living in and working from Brussels. In the month of September 2024, I'll be splitting time between London and other parts of the U.K., and Italy where I'll be working with clients on consumer health, self-care and home care focused on food-as-medicine, digital health, business and scenario planning for the future...

As you may know, I have been splitting work- and living-time between the U.S. and the E.U., most recently living in and working from Brussels. In the month of September 2024, I'll be splitting time between London and other parts of the U.K., and Italy where I'll be working with clients on consumer health, self-care and home care focused on food-as-medicine, digital health, business and scenario planning for the future...