The Direct Link Between Value-Based Health Care, Digital Transformation and Social Determinants – Insights from Innovaccer and Morning Consult

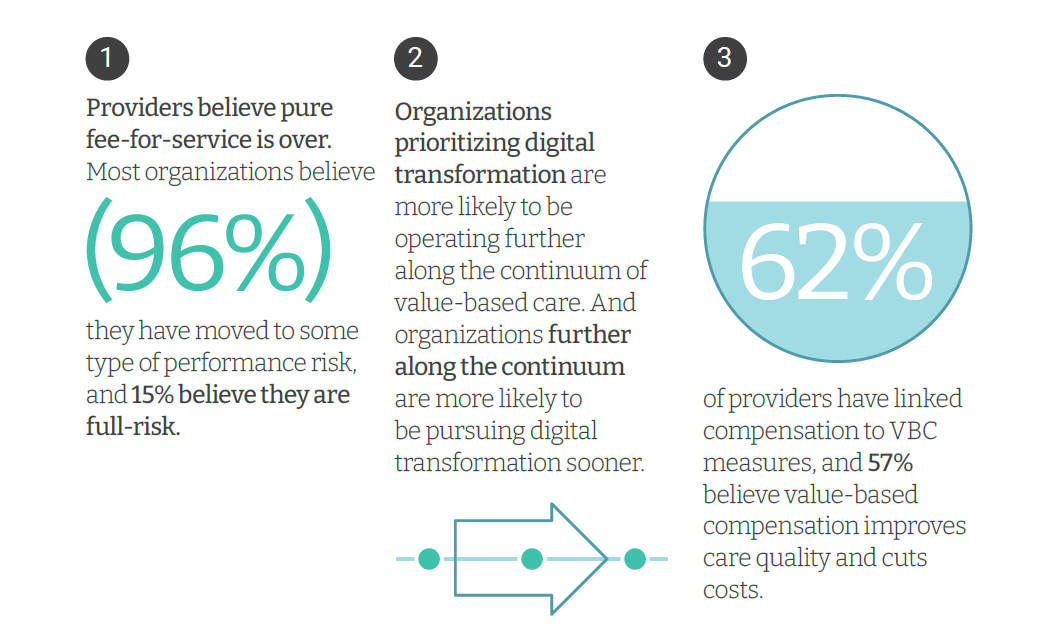

Only 4% of health care payments in the U.S. are pure fee-for-service (FFS) these days. “The end of pure FFS is near,” according to The State and Science of Value-Based Care, a report-out of survey research from Innovaccer and Morning Consult. Innovaccer, a health cloud/data analytics company, worked with Morning Consult to do deep-dive interviews with 75 senior health care executives; research was conducted in November and December 2021, so these perspectives represent those of health system leaders at the start of 2022. The full report is worth your read; my focus in this Health

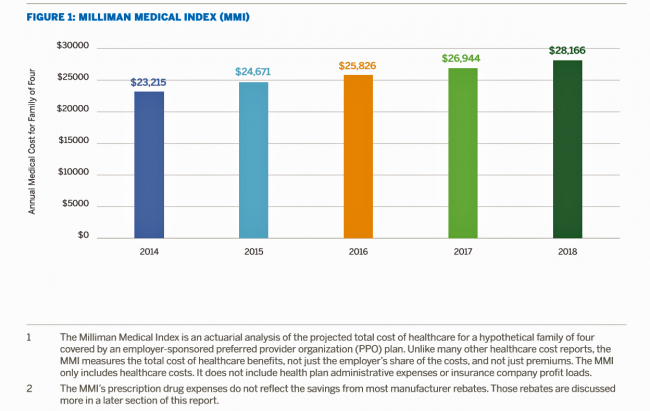

Health Care for a Typical Working Family of Four in America Will Cost $28,166 in 2018

What could $28,166 buy you in 2018? A new car? A year of your child’s college education? A plot of land for your retirement home? Or a year of healthcare for a family of four? Welcome to this year’s edition of the Milliman Medical Index (MMI), one of the most important forecasts of the year in the world of the Health Populi blog and THINK-Health universe. That’s because we’re in the business of thinking about the future of health and health care through the health economics lens; the MMI is a key component of our ongoing environmental analysis of the

Employers Changing Health Care Delivery – Health Reform At Work

Large employers are taking more control over health care costs and quality by pressuring changes to how care is actually delivered, based on the results from the 2017 Health Plan Design Survey sponsored by the National Business Group on Health (NBGH). Health care cost increases will average 5% in 2017 based on planned design changes, according to the top-line of the study. The major cost drivers, illustrated in the wordle, will be specialty pharmacy (discussed in yesterday’s Health Populi), high cost patient claims, specific conditions (such as musculoskeletal/back pain), medical inflation, and inpatient care. To temper these medical trend increases,

Accountable Care Will Happen Best When Patients Engage

Technology alone won’t improve health care in America, especially in people with chronic health problems don’t want to use it. Furthermore, too many clinicians who have invested in digital health technologies (namely, electronic health records systems), aren’t fully taking advantage of what they have. This and other health care realities are explored in Better Together: Patient Expectations and the Accountability Gap, based on a consumer survey conducted by Nielsen Strategic Health Perspectives for the Council of Accountable Physician Practices, an affiliate of the American Medical Group Foundation. The survey polled 30,007 consumers in March 2016, and combined physician data culled from Nielsen’s

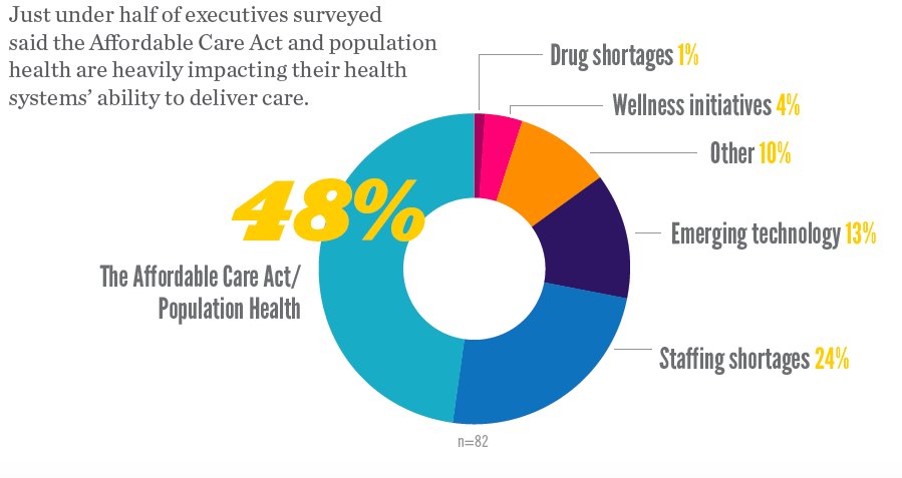

The Hospital of the Future Won’t Be a Hospital At All

In the future, a hospital won’t be a hospital at all, according to 9 in 10 hospital executives who occupy the c-suite polled in Premier’s Spring 2016 Economic Outlook. Among factors impacting their ability to deliver health care, population health and the ACA were the top concerns among one-half of hospital executives. 1 in 4 hospital CxOs think that staffing shortages have the biggest impact on care delivery, and 13% see emerging tech heavily impacting care delivery. Technology is the top area of capital investment planned over the next 12 months, noted by 84% of hospital execs in the survey.

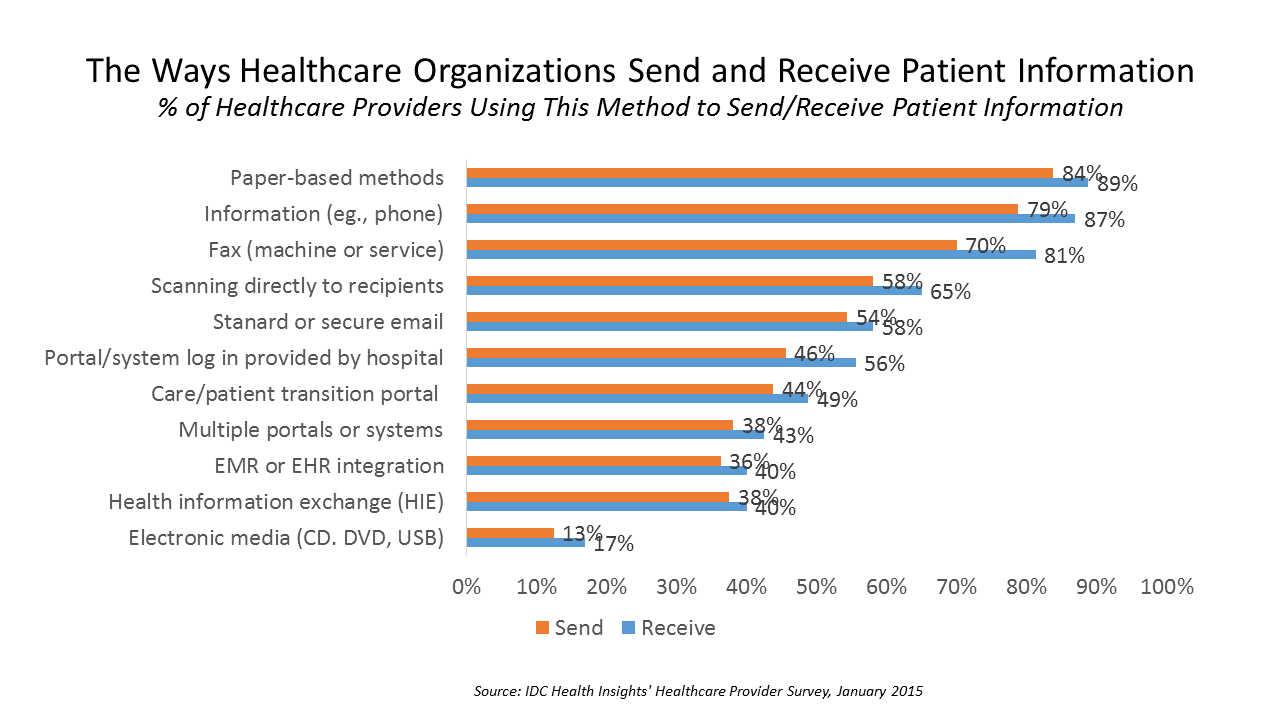

Paper and Fax, Not EHRs or Portals, Are Popular for Health Data Sharing

Faxing in health care ranks higher in patient data information sharing than using secure email, online portals, health information exchange (HIE), or leveraging electronic health records. Welcome to the American healthcare system in 2016, as described in a market spotlight published by IDC, The Rocky Road to Information Sharing in the Health System. IDC’s survey research among healthcare providers forecasts the “rocky road” to information sharing. That rocky road is built for medical errors, duplication of services, greater healthcare costs, and continued health il-literacy for many patients. “The holy grail of interoperability — lower-cost, better-quality care with an improved experience for

Virtual Visits Would Conserve Primary Care Resources in US Healthcare

By shifting primary care visits by 5 minutes, moving some administrative tasks and self-care duties to patients, the U.S. could conserve billions of dollars which could extend primary care to underserved people and regions, hire more PCPs, and drive quality and patient satisfaction. Accenture’s report, Virtual Health: The Untapped Opportunity to Get the Most out of Healthcare, highlights the $10 bn opportunity which translates into conserving thousands of primary care providers. PCPs are in short supply, so virtual care represents a way to conserve precious primary care resources and re-deploy them to their highest-and-best-use. The analysis looks at three scenarios

The Tricky Journey From Volume To Value In Health Care – Prelude To Health 2.0

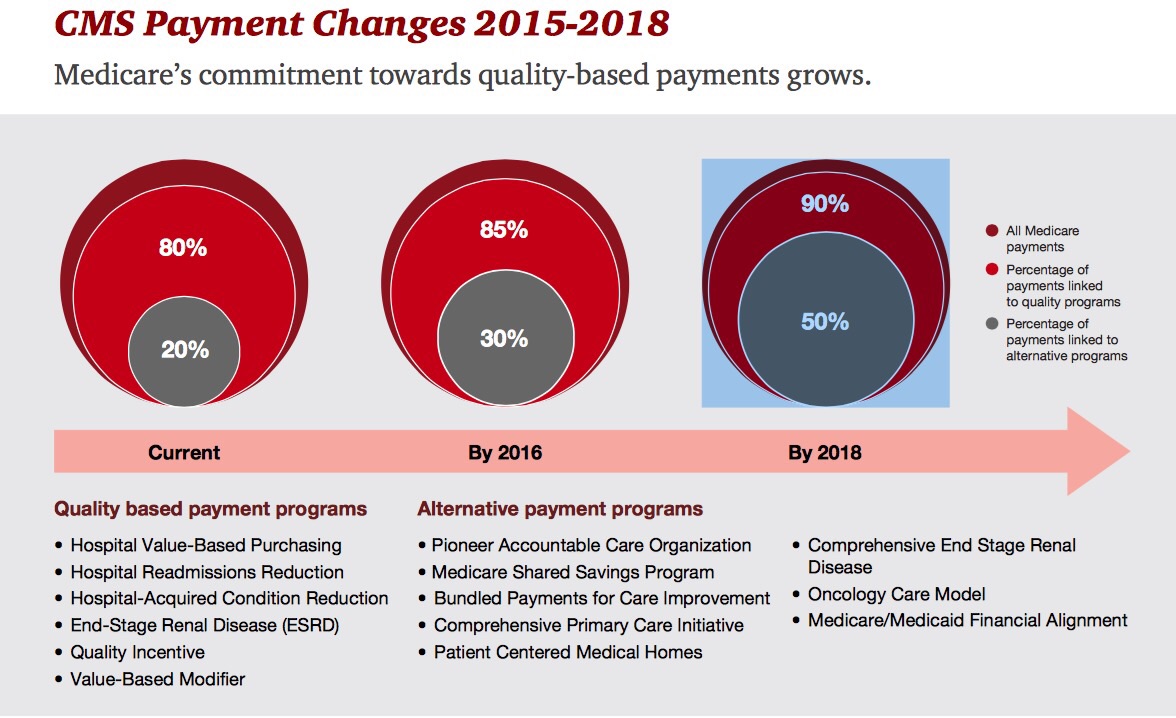

By 2018, 90% of health care delivered to people enrolled in Medicare will be paid-for on the basis of quality, not on the amount of services delivered (that is, volume). But as providers must up their game in that new value-oriented health payment world, they are bound up in work flows and organizational structures built for fee-for-service reimbursement. This changing future is discussed in Healthcare’s alternative payment landscape, PwC’s Healthcare Research Institute report on the volume-to-value shift. PwC notes that health care providers’ ability to adapt to changing payment regimes vary and fall into four categories: traditional, lagging, vanguard and

Risk-shift: employers continue to push more risk to employees and families for health costs

With health costs increase increasing at 4.4% in 2014, a slightly higher rate of growth than the 4.1% seen in 2013. While this is lower than the double-digit increases U.S. employers faced in 2001-2004, it’s still twice the rate of general consumer price inflation. That’s what the first graph shows, based on the The 19th Annual Towers Watson/National Business Group on Health Employer Survey on Purchasing Value in Health Care. Employers generally want to continue to provide health insurance…for the time being. 92% of companies expect to make changes in health plan provisions in 2014, with 1 in 2 anticipating “significant

Health Care Everywhere at the 2014 Consumer Electronics Show

When the head of the Consumer Electronics Association gives a shout-out to the growth of health products in his annual mega-show, attention must be paid. The #2014CES featured over 300 companies devoted to “digital health” as the CEA defines the term. But if you believe that health is where we live, work, play, and pray, then you can see health is almost everywhere at the CES, from connected home tech and smart refrigerators to autos that sense ‘sick’ air and headphones that amplify phone messages for people with hearing aids, along with pet activity tracking devices like the Petbit. If

Innovating and thriving in value-based health – collaboration required

In health care, when money is tight, labor inputs like nurses and doctors stretched, and patients wanting to be treated like beloved Amazon consumers, what do you do? Why, innovate and thrive. This audacious Holy Grail was the topic for a panel II moderated today at the Connected Health Symposium, sponsored by Partners Heathcare, the Boston health system that includes Harvard’s hospitals and other blue chip health providers around the region. My panelists were 3 health ecosystem players who were not your typical discussants at this sort of meeting: none wore bow ties, and all were very entrepreneurial: Jeremy Delinsky

A new medical side-effect: out-of-pocket health care costs

When we say the phrase “side effects,” what do we think of? The FDA says that “all medicines have benefits and risks. The risks of medicines are the chances that something unwanted or unexpected could happen to you when you use them. Risks could be less serious things, such as an upset stomach, or more serious things, such as liver damage.” There’s a new risk in town in health care, and it’s the equivalent of an upset stomach when it comes to a co-pay for a branded on-formulary drug, or liver damage if it involves a coinsurance percent of “retail”

The slow economy is driving slower health spending; but what will employers do?

By 2022, $1 in every $5 worth of spending in the U.S. will go to health care in some way, amounting to nearly $15,000 for each and every person in America. From biggest line item on down, health spending will go to payments to: Hospitals, representing about 32% of all spending Physicians and clinical costs, 20% of spending Prescription drugs, 9% of spending Nursing, continuing care, and home health care, together accounting for over 8% of health spending (added together for purposes of this analysis) Among other categories like personal care, durable medical equipment, and the cost of health insurance.

Healing the Patient-Doctor Relationship with Health IT

A cadre of pioneering Americans has been meaningfully using personal health information technology (PHIT), largely outside of the U.S. health care system. These applications include self-tracking and wearable health technologies, mobile health apps, and digital medical tracking devices like glucometers that streamline tracking and recording blood glucose levels. In the meantime, only 21% of doctors surveyed by Accenture currently allow patients to have online access to their medical summary or patient chart – very basic components of the electronic health record. We know what’s primarily driving health providers’ adoption of health IT: namely, the HITECH Act’s provisions for incentives. But

People with doctors interested in EMRs, but where’s the easy button?

1 in two people who are insured and have a regular doctor are interested in trying out an electronic medical record. But they need a doctor or nurse to suggest this, and they need it to be easy to use. The EMR Impact survey was conducted by Aeffect and 88 Brand Partners to assess 1,000 U.S. online consumers’ views on electronic medical records (EMRs): specifically, how do insured American adults (age 25 to 55 who have seen their regular physician in the past 3 years) view accessing their personal health information via EMRs? Among this population segment, 1 in 4 people (24%)

Working for health care in 2013: workers’ health insurance cost burden still grows faster than wages

Insurance premium costs grew 4% for families between 2012 and 2013, with workers now bearing 39% of health premiums in 2013 compared with only 26% ten years ago, in 2003. That’s a 50% increase in health plan premium “burden” for working families, by my calculation. This snapshot of health insurance in 2013 comes to us from the 2013 Employer Health Benefits Survey, provided by the Kaiser Family Foundation (KFF) and the Health Research & Educational Trust (HRET). This research is one of the most important annual reports to hit the health care industry every year, and this year’s analysis provides strategic context

In the US health care cost game, doctors have seen the enemy – and it’s not them

When it comes to who’s most responsible for reducing the cost of health care in America, most doctors put the onus on trial lawyers, health insurance companies, pharma and medical device manufacturers, hospitals, and even patients. But physicians themselves ? Not so much responsibility – only 36% of doctors polled said doctors should assume major responsibility in reducing health care costs. And, in particular, most U.S. physicians have no enthusiasm for reducing health care costs by changing payment models, like penalizing providers for hospital re-admissions or paying a group of doctors a fixed, bundled price for managing population health. Limiting

Urgent care centers: if we build them, will all patients come?

Urgent care centers are growing across the United States in response to emergency rooms that are standing-room-only for many patients trying to access them. But can urgent care centers play a cost-effective, high quality part in stemming health care costs and inappropriate use of ERs for primary care. That’s a question asked and answered by The Surge in Urgent Care Centers: Emergency Department Alternative or Costly Convenience? from the Center for Studying Health System Change by Tracy Yee et. al. The Research Brief defines urgent care centers (UCCs) as sites that provide care on a walk-in basis, typically during regular

They call it “primary” care because it comes first — and it should

It’s called “primary” care for a reason: it’s first and foremost important in the health care services a person can use. In its report, Primary care: our first line of defense, The Commonwealth Fund explains why primary care is crucial to one’s individual health, and how primary care is morphing into medical teams and patient-centered medical homes. And that’s a good thing for you and me, the Fund says. That’s because people in the U.S. who have a primary care doctor have 33% lower health costs and 19% lower risk of dying than people who see only a specialist (Source:

The part-time medical home: retail health clinics

The number of retail health clinics will double between 2012 and 2015, according to a research brief from Accenture, Retail medical clinics: From Foe to Friend? published in June 2013. What are the driving market forces promoting the growth of retail clinics? Accenture points to a few key factors: Hospitals’ need to rationalize use of their emergency departments, which are often over-crowded and incorrectly utilized in cases of less-than-acute care. In addition, hospitals are now financially motivated under the Affordable Care Act (ACA, health reform) to reduce readmissions of patients into beds (particularly Medicare patients with acute myocardial infarction [heart attacks],

Bending the cost-curve: a proposal from some Old School bipartisans

Strange political bedfellows have come together to draft a formula for dealing with spiraling health care costs in the U.S. iin A Bipartisan Rx for Patient-Centered Care and System-Wide Cost Containment from the Bipartisan Policy Center (BPC). The BPC was founded by Senate Majority Leaders Howard Baker, Tom Daschle, Bob Dole, and George Mitchell. This report also involved Bill Frist, Pete Domenici, and former White House and Congressional Budget Office Director Dr. Alice Rivlin who together work with the Health Care Cost Containment Initiative at the BPC. The essence of the 132-page report is that the U.S. health system is

A health economics lesson from Jonathan Bush, at the helm of athenahealth

At HIMSS13 there are the equivalent of rock stars. Some of these are health system CIOs and health IT gurus who are driving significant and positive changes in their organizations, like Blackford Middleton, Keith Boone, Brian Ahier, and John Halamka. Others are C-level execs at health IT companies. In this latter group, many avoid the paparazzi (read: health trade reporters) and stay cocooned behind closed doors in two-story pieces of posh real estate on the exhibition floor. A few walk the floor, shake hands with folks, and take in the vibe of the event. We’ll call them open-source personalities. The

The future of sensors in health care – passive, designed, integrated

Here’s Ann R., who is a patient in the not-too-distance-future, when passive sensors will be embedded in her everyday life. The infographic illustrates a disruption in health care for people, where data are collected on us (with our permission) that can help us improve our own self-care, and help our clinicians know more about us outside of their offices, exam rooms and institutions. In Making Sense of Sensors: How New Technologies Can Change Patient Care, my paper for the California HealthCare Foundation, I set out to organize the many types of sensors proliferating the health care landscape, and identify key

The Accountable Care Community opportunity

“ACOs most assuredly will not…deliver the disruptive innovation that the U.S. health-care system urgently needs,” wrote Clay Christensen, godfather of disruptive innovation, et. al., in an op-ed in the Wall Street Journal of February18, 2013. In the opinion piece, Christensen and colleagues make the argument that Accountable Care Organizations (ACOs) as initially conceived won’t address several key underlying forces that keep the U.S. health care industry in stasis: Physicians’ behavior will have to change to drive cost-reduction. Clinicians will need “re-education,” the authors say, adopting evidence-based medicine and operating in lower-cost milieus. Patients’ behavior will have to change. This requires

The more engaged a patient is, the lower their costs

There are many ways to measure and express “patient engagement.” One such metric is “patient activation,” innovated by Dr. Judith Hibbard, long affiliated with the University of Oregon. Dr. Hibbard has written extensively about the Patient Activation Measure, PAM, first described in 2004. She and a team of researchers have determined that the higher a patient’s PAM score, the lower their health costs. Hibbard et. al. published these findings in the February 2013 issue of Health Affairs, which is entirely devoted to patient engagement – a top topic in Health Populi. The team analyzed the medical records of 33,163 patients

Americans #1 health care priority for the President: reduce costs

Reducing health care costs far outranks improving quality and safety, improving the public’s health, and upping the customer experience as Americans’ top priority for President Obama’s health care agenda, according to a post-election poll conducted by PwC’s Health Research Institute. In Warning signs for health industry, PwC’s analysis of the survey results, found that 7 in 10 Americans point to the high costs of health care as their top concern in President Obama’s second term for addressing health care issues. Where would cost savings come from if U.S. voters wielded the accountant’s scalpel? The voters have spoken, saying, Reduce payments

Employers slow health cost increases for 2013 by growing consumer-directed plans

Health benefit costs grew a relatively low 4.1% in 2012 (5.4% for large employers), largely due to companies moving workers into lower-cost consumer-directed health plans. Last year, benefit costs grew at an annual rate of 6.1%, representing about a 30% fall in year-on-year cost growth for companies. And, coverage is up to 59% of employees having ticked down to 55% for the past couple of years. Employers expect about a 5% increase for 2013. Mercer’s National Survey of Employer-Sponsored Health Plans analysis finds that U.S. employers are looking toward 2014, when they’ll be covering more uninsured workers, and using this advance

Pharmacists are a valuable member of the primary care team

It’s American Pharmacist Month, so let’s celebrate that key member of the health care team. Most Americans live quite close to a pharmacy, compared with peoples’ proximity to doctors, hospitals and emergency rooms. The pharmacist is not only a trusted health professional in the eyes of consumers: he/she is a key influencer on peoples’ health. And seeing as the #1 barrier to people taking prescription drugs is cost, the community-based pharmacist is in a prime position to educate, influence and motivate people to become more informed and activated health consumers. CVS Caremark’s survey of pharmacists is discussed in the company’s

In this Age of the Healthcare Consumer, most people want online access to doctors and health records

Just as people go online for travel planning. photo development. and financial transactions. they’re looking for health engagement with their doctors and health records online, too. Harris Interactive heralds this as The Age of the Healthcare Consumer. Harris Interactive polled U.S. adults and found that people are interested in a range of technologies for engaging in their health, arrayed in the chart: when asked which would be important for health providers to implement, consumers said (NET = very important + important): – Online medical record access to visits, Rx, test results, and history, 65%. 17% of consumers said their doctor

Aetna finds consumers aren’t very empowered in health

Americans find health insurance decisions the second most difficult major life decision only behind saving for retirement (36%) and slightly more difficult than purchasing a car (23%), via Aetna’s Empowered Health Index Survey. Why are health insurance choices so tough? Consumers told Aetna that the available information is confusing and complicated (88% percent), there is conflicting information (84%) and it’s difficult to know which plan is right for them (83%). Based on this survey’s findings, millions of Americans indeed feel dis-empowered by health care decision making. Who is empowered? Aetna says the empowered are likely to be more affluent, insured, married, take

The rise and rise of retail clinics: a growing site for primary care, everywhere

There were nearly 6 million patient visits to retail health clinics in 2009. Such visits to retail clinics rose four-fold between 2007 and 2009, according to a RAND study published in the September 2012 issue of Health Affairs. Visits for prevention versus acute care in 2009 were roughly evenly split, with 47.5% and 51.4% of people over 18 seeking prevention vs. acute care from retail clinics, respectively. The most common acute care complaints in the retail setting were upper respiratory infections, pharyngitis, otitis externa, conjunctivitis, urinary tract infections, and allergies. What’s underneath the impressive rise is important to parse out

Physicians not doing so well – financially, socially, physically – and what it means for health reform

Physicians’ wellbeing dropped in July: while providers’ mental health stayed sound since June, it’s financial, physical and social health that’s dragging providers’ overall wellness down. QuantiaMD, the social network exclusively for doctors, launched the Physician Wellbeing Index in January 2012. The Index measures four aspects of physician-reported wellbeing: physical, mental, financial, and social health. QuantiaMD says it’s the world’s only measure of “how physicians are doing as people.” Based on the Index, QuantiaMD tailors content to meet the needs of the physicians in the social network. In July, the chart illustrates that doctors’ wellbeing slipped in 3 of the 4

Why we now need primary care, everywhere

With the stunning Supreme Court 5-4 majority decision to uphold the Patient Protection and Affordable Care Act (ACA), there’s a Roberts’ Rules of (Health Reform) Order that calls for liberating primary care beyond the doctors’ office. That’s because a strategic underpinning of the ACA is akin to President Herbert Hoover’s proverbial “chicken in every pot:” for President Obama, the pronouncement is something like, “a medical home for every American.” But insurance for all doesn’t equate to access: because 32-some million U.S. health citizens buy into health insurance plans doesn’t guarantee every one of them access to a doctor. There’s a

The pharmaceutical landscape for 2012 and beyond: balancing cost with care, and incentives for health behaviors

Transparency, data-based pharmacy decisions, incentivizing patient behavior, and outcomes-based payments will reshape the environment for marketing pharmaceutical drugs in and beyond 2012. Two reports published this week, from Express Scripts–Medco and PwC, explain these forces, which will severely challenge Pharma’s mood of market ennui. Express-Scripts Medco’s report on 9 Leading Trends in Rx Plan Management presents findings from a survey of 318 pharmacy benefit decision makers in public and private sector organizations. About one-half of the respondents represented smaller organizations with fewer than 5,000 employees; about 20% represented jumbo companies with over 25,000 workers. The survey was conducted in the

The economics of being a practicing physician: greater frustration, lower income, more defensive

One-half of physicians believe they’re not fairly compensated for their work – in particular, those working in primary care. Only 11% of doctors considering themselves “rich.” Medscape’s 2012 Physician Compensation Report compiled data from over 24,000 U.S. physicians across 24 specialties and found the bulk of physicians to see themselves working harder and 1 in 4 making less money than last year. This has led to growing frustration and worry, where some physicians are resenting the large pay gap between specialists and primary care. That frustration looks poised to increase with doctors concerned that accountable care will further eat into

Patient engagement and medical homes – core drivers of a high-performing health system

It was Dr. Charles Safran who said, “Patients are the most under-utilized resource in the U.S. health system,” which he testified to Congress in 2004. Seven years later, patients are still under-utilized, not just in the U.S. but around the world. Yet, “when patients have an active role in their own health care, the quality of their care, and of their care experience improves,” assert researchers from The Commonwealth Fund in their analysis of 2011 global health consumer survey data published in the April/June 2010 issue of the Journal of Ambulatory Care Management. This analysis is summarized in International Perspectives on

Under 10% of people manage health via mobile: a reality check on remote health monitoring from HIMSS

With mobile health consumer market projections for ranging from $7 billion to $43 billion, according to PricewaterhouseCoopers, a casual reader might think that a plethora of health citizens are tracking their health, weight, food intake, exercise, and other observations of daily living by smartphones and tablets. But as the chart shows, health self-trackers number around 1 in 20 U.S. adults, according to a survey conducted for HIMSS Analytics and sponsored by Qualcomm Life. HIMSS Analytics’ report, A New Prescription for Chronic Disease: remote monitoring devices, was published in conjunction with the annual HIMSS conference which highlights the latest health information technology

Consumers are at the center of the business of health and wellness

The market for health and wellness has traditionally included over-the-counter medicines, gym memberships, and vitamins/minerals/supplements. In 2012, the boundaries of health/wellness are blurring beyond these line items toward preventive medical services and consumer electronics. This morphing market is discussed by Cambridge Consultants in their report on the disruptions driving The Business of Health & Wellness: Engaging consumers and making money. Cambridge correctly introduces this analysis by saying that economics, the growing prevalence of chronic diseases, an aging population, and demand consumers are shaping health/wellness, “recharacterizing” the market as one driven by “life events.” Cambridge sees that health consumers are changing their spending

Primary care, everywhere: how the shortage of PCPs is driving innovation – especially for patient participation in their own care

The signs of the primary care crisis in America are visible: A growing number of visits to the emergency room for treating commonplace ailments Waiting lists for signing up with and queuing lines to see primary care doctors Fewer med students entering primary care disciplines Maldistribution of primary care practitioners (PCPs) in underserved areas, rural, exurban and urban. The implementation of the Affordable Care Act will (try to) enroll at least 30 million newly-insured health citizens into the U.S. health system. That’s the objective: whether being insured will actually provide people access to needed primary care is a big question given the current supply of

Get into the sunshine, church is out – the GAO report on health care price transparency

This morning during my still-dark-at-5:15 am walk, my iPod was motivating me to “get up offa that thing,” as James Brown was motivating me to “release the pressure.” Two minutes into the song, he urges, “Get into the sunshine, church is out.” This brought to mind a publication I’ve taken time to review from the General Accounting Office (GAO) report to the U.S. Congress, Health Care Price Transparency – Meaningful Price Information Is Difficult for Consumers to Obtain Prior to Receiving Care, published in September 2011. While employers and health plans want consumers to become more engaged in their health, a key barrier facing

Interviewed live on BNN Bloomberg (Canada) on the market for GLP-1 drugs for weight loss and their impact on both the health care system and consumer goods and services -- notably, food, nutrition, retail health, gyms, and other sectors.

Interviewed live on BNN Bloomberg (Canada) on the market for GLP-1 drugs for weight loss and their impact on both the health care system and consumer goods and services -- notably, food, nutrition, retail health, gyms, and other sectors. Thank you, Feedspot, for citing the Health Populi blog as one of the best in the field this year! Very grateful to be among the company of some of my own go-to's such as Everyday Health, NPR Health Shots, Health Affairs, and Kaiser Health News, among others...

Thank you, Feedspot, for citing the Health Populi blog as one of the best in the field this year! Very grateful to be among the company of some of my own go-to's such as Everyday Health, NPR Health Shots, Health Affairs, and Kaiser Health News, among others... As you may know, I have been splitting work- and living-time between the U.S. and the E.U., most recently living in and working from Brussels. In the month of September 2024, I'll be splitting time between London and other parts of the U.K., and Italy where I'll be working with clients on consumer health, self-care and home care focused on food-as-medicine, digital health, business and scenario planning for the future...

As you may know, I have been splitting work- and living-time between the U.S. and the E.U., most recently living in and working from Brussels. In the month of September 2024, I'll be splitting time between London and other parts of the U.K., and Italy where I'll be working with clients on consumer health, self-care and home care focused on food-as-medicine, digital health, business and scenario planning for the future...